{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

These Related Episodes

Featuring

Michael Kitces

Co-Founder, XYPN

Alan Moore

CEO & Co-Founder, XYPN

UPDATE: We've published a deeper dive into the stats HERE!

What does it look like to scale your RIA and how long does it take? How big of an impact does it really make to have a niche? When should you start hiring, and who should it be when you do?

Co-Founders Alan Moore and Michael Kitces met onstage this year to review the highlights of the seventh-annual Member Benchmarking Study in this episode of XYPN Radio. Every year, the study gathers information from XYPN member participants to get an accurate picture of how advisors are doing in their firms.

This episode tells the story of how XYPN firms are scaling and what to look out for in your own journey. Whether you’re getting ready to launch, are in your first years, or are already established, this is an episode you won’t want to miss.

.png?width=1200&height=300&name=XYPN%20Radio%20Blog%20signature%20(1).png)

Listen to the Full Interview:

Watch the Full Interview:

1. What the benchmarking study is and how it is conducted (1:04)

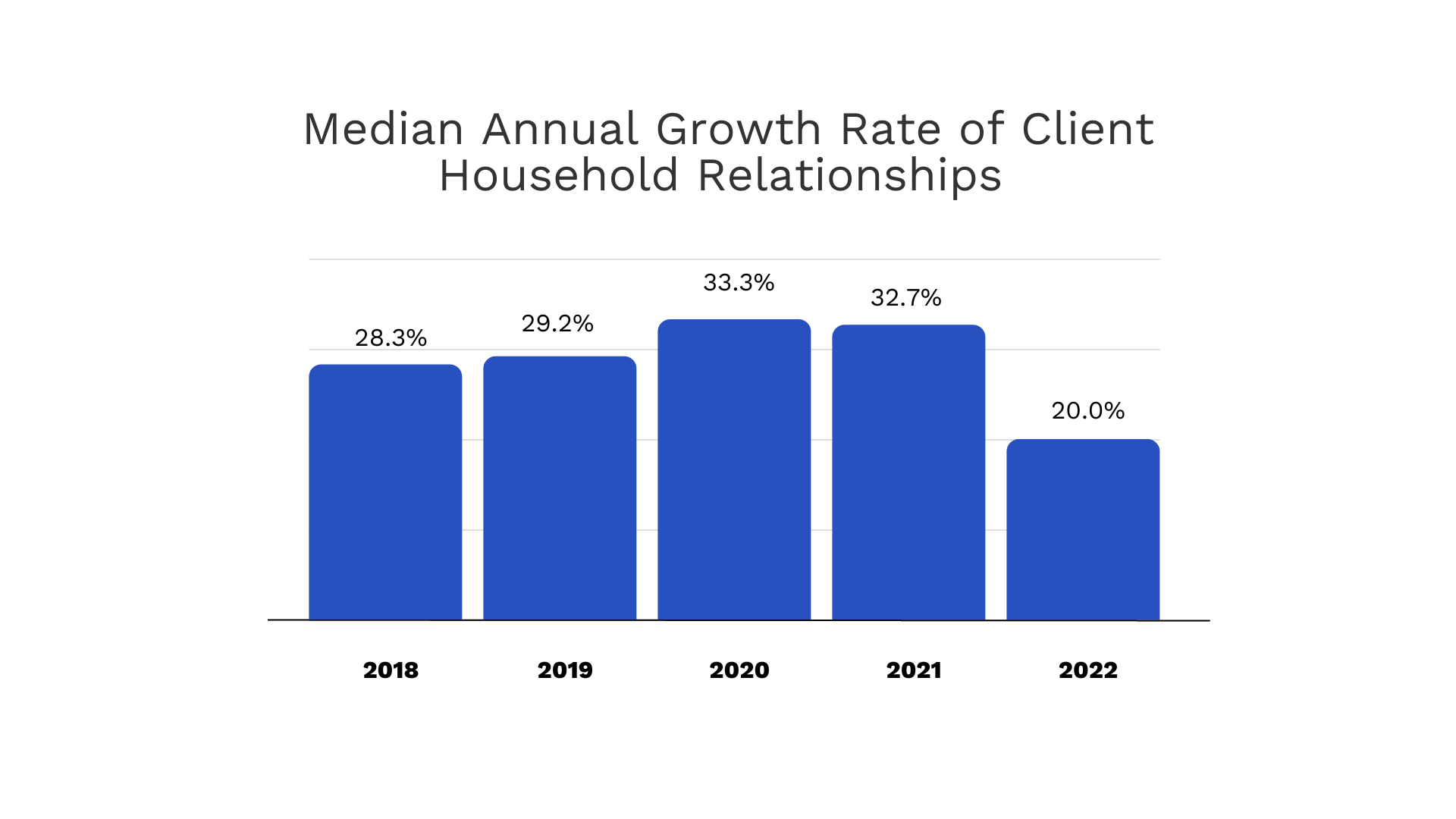

2. The median annual growth rate of client relationships since 2018. Unlike other figures that largely are talking about AUM, this gives a real snapshot of growth rates of fee for service models. Alan and Michael discuss how fee for service models stand up to economic cycles and interest rates as seen over the last seven years (2:33)

3. Average annual revenue for those who join with few to no clients. We want to be realistic when we tell you what to expect as you start your firm and have the data to back it up! Alan and Michael discuss what the data means and how it shapes those pivotal early years (16:37)

4. Revenue growth by niche vs no niche. Broken up by Implementation (0-20 clients), Building (20-75 clients), and Scaling (75 client households and/or 150K revenue) phases. (23:46)

5. Percentage of Advisors leveraging in-house or outsourced staff and number of clients. For someone looking to hire, this is an important one! (37:55)

6. Staff productivity by business type. Whether you have a solo, boutique, or enterprise practice, we take a look revenue per advisor as staff gets added to the business. (49:15)

Featured on the Show:

- Chartered Financial Analyst®

- Certified Financial Planner™

- Compound Annual Growth Rate (CAGR)

- XYPN LIVE

- Chart 1 - The median annual growth rate of client relationships since 2018.

- Chart 2 - Average annual revenue for members who join with few clients.

- Chart 3 - 2022 Revenue growth by niche focus for members joining with few clients

- Chart 4 - Percentage of Advisors leveraging in-house or outsourced staff and number of clients.

- Chart 5 - Staff productivity by business type for scaling a business

This Episode Is Sponsored By:

Read the Transcript Below:

Alan Moore: Hello and welcome to this episode of XYPN Radio. I am your host, Alan Moore, and I'm excited to have my co host Michael Kitces here with me. Talking about our 2022, I always get this wrong, 2023 benchmarking survey, 2022 data. So thanks for joining me.

Michael Kitces: I'm excited to be here. And I, yeah, I feel like we have to clarify the confusion.

It's like 2023 benchmarking study, cause that's when we put it out. Just happens to be the 2022 data because, you know, we can't really say how this year's going until the year's over and it's not over yet.

Alan Moore: That is true. So we every year we collect data from our members which is really the largest study that I'm aware of that's done with independent research. Looking at fee for service financial advisors, really getting an understanding of, you know, how are they growing their businesses?

What does revenue look like over time, client growth, you know, productivity measures. There's a whole slew of questions that we ask to really gather a lot of data to be able to analyze. You know, basically what is helping them, you know, build their successful practices. This year was actually the first year we moved our data collection process.

We used to basically use a survey monkey type form and we ended up moving it into our internal technology for members, which really increased participation. So this year I believe participation was up about 70% or something like that from years prior. So we got a lot more data, a lot more information to be able to contribute just to be sure that we're getting you know, well rounded representation. So, for listeners we're going to be talking a lot about charts and graphs. I'm going to do my best to paint the picture with my words, but I'm looking at the charts and I know that's a little different. So if you go to XYPlanningNetwork.com/373. You'll be able to look at the, about five charts depending on time. About five charts that we'll get to and be able to talk about.

Michael Kitces: It's like you've thrown down the gauntlet for me. Can we get through five charts?

Alan Moore: Can we get through five in less than an hour? We shall see. All right, so the first interesting takeaway that we had from the benchmarking survey references our first graph in the benchmarking survey, which is the median annual growth rate of client household relationships since 2018.

So first off, I guess in your mind, why do we look at client households versus revenue or assets under management, which is what most of the industry is looking at in these studies?

Michael Kitces: It's a good question. So, for context, right? If you look at most industry benchmarking studies, when most studies talk about like, the average growth rate of a firm, right? Just sort of like, they throw that number out there, advisory firms that had grown at a rate of blank. Virtually all of them are talking about growth in assets under management.

In the context of fee for service, to me that just like, that doesn't work cause like it, it just literally doesn't speak to the economic health and status of a lot of advisory firms operating fee for service. Cause either their advice only like, "Well my growth rate was infinity because I grew from zero to zero", like not helpful.

Or even just a lot of firms that have blended models are predominantly subscription fee models. Looking at your assets is not particularly representative of the growth and the health of the business. So to me just AUM... I mean look, if you're 100% assets under management that's your model, like, fine way to measure.

But just from a big benchmarking, what's the health of growth perspective, AUM just literally doesn't work in fee for service. The second way to look at this is revenue and looking at growth of revenue from all the different places that we get revenue sources. And we actually do have some numbers in like the appendix to the study that looks at revenue as well.

I do think revenue growth is a really good way to look at health of advisory firms overall and how firms are growing, right? It's literally the dollars that we're bringing in and we can understand what's happening with growth. My particular interest in this, when we look at sort of overall, like, how is the network growing? Is to understand clients that are coming in, right?

In the purest sense, in an AUM firm, a lot of growth actually has nothing to do with new clients coming on board. It's "My revenue went up because the markets went up and I bill as a percentage of assets. So when markets go up, assets go up and my revenue goes up." Fine thing in terms of overall like profits of the firm. But you know, I've seen a lot of advisory firms over the years that are like, "Yeah, we've been doing great! We've been growing at 10-15% a year for the past five years!" I'm like, we're in a fricking bull market. Like, the markets are up 10-15% a year over the past five years. So if you tell me you're up 10-15%, that basically means you probably have added like one client in the past five years.

Fine, if that's how you want to run your business and you're at a good revenue point, but like not a great way to really understand health of the business and growth of the business. So to me, the sort of purest, simplest measure to understand what growth looks like is, "Are new clients coming in?".

Are we signing new client households? Are we adding to the client headcount? And to me, that's sort of one of the purest equalizers across firms, across models, across types. So, like, that's why we look at it from a pure business perspective. I think there is also a lot of value in looking at revenue growth. And I encourage anyone, like, looking at health of their practice, revenue growth is a good thing to look at.

But even if you're thinking about revenue growth in the purest sense. Like, break it out into what is my revenue growth from new clients and what is my revenue growth from existing clients, right? If I'm assets under management, they added assets. If I'm subscription fee, I raised my fees or they moved up tiers. If I've got tiers and they moved to a higher tier. It's always important to understand the breakdown of your revenue growth between new revenue from new and new revenue from existing, in kind of the purest sense. But to me, like when we're looking at what's going on with XYPN overall, I just, I continue to be intrigued by just flat out, how many new clients are getting signed up?

Alan Moore: And one of the beauties of having done this study now, I believe it's six, maybe seven years. It's been, we've been doing this for a long, long time now is that we have some, we have the data so that, you know, folks aren't having to report five years ago. We're able to collect this data over time and sort of see. Things like you know, again, this chart speaking to the median annual growth rate of the client household.

So basically, how many more, what percentage of new households did the did the advisor add in the last 12 months? And so you know, if you go back to 2018, it was 28%. 2019 was 29%. 2020 and 2021 we're about 33%. And then 2022 did come down, but it was still 20% in terms of growth. And I believe what we said over five years, that averages to about 28% year over year growth for five years.

Michael Kitces: Yeah, compound average annual growth rate is just about 29.

Alan Moore: I would say CAGR, but no one actually knows what CAGR means.

Michael Kitces: CAGR! Like "Compound Annual Growth Rate" yeah. You know, when I look at this number overall, I mean, it was interesting. So over the years, there was a lot of discussion around, and frankly even like core criticisms in the direction of XYPN and the subscription model in general- "Well, are, like, are people going to stay around when, like, when markets get turbulent, and the economy gets turbulent. Is anyone going to, going to stick around? And so it was fascinating me to see in practice, like as we went through 2019, 2020, pandemic volatility, 2021, overall economic volatility and layoffs. It was like ,no! Basically like had no, no measurable effect. In fact as we highlight in the data, client growth rates were actually a little bit better into 2021, 2020 and 21 during the pandemic than they were before. But then we did see at least a, relative growth slowdown in, in 2022, and what, what strikes me, like I, I can sort of see what happened in practice and just knowing like a lot of our member firms and the challenges that they went through over the past year.

So it turns out, at least as XYPN members tend to build their firms, not so sensitive to market cycles and market volatility, not even quite as sensitive to economic cycles and like economic volatility. But it turns out we are actually remarkably sensitive to interest rates. Go figure, there's like an interest rate sensitivity thing that ripples through who XYPN members serve. In the purest sense, like interest rates went up. What happened is interest rate went up, cost of capital got more expensive. What happened is cost of capital got more expensive, slowdown in acquisitions by venture capital and PE firms, slowdown in new investments. General slowdown in mergers and acquisitions across lots of industries, big slowdown in IPOs over the past year.

And so not true of all members, but there are a non trivial segment of members that are in some way, shape, or form attached to people that have liquidity events, that are attached to VC, PE, IPO related things, right? That's a moment of financial and wealth complexity that makes stuff happen that says, "Oh my gosh, I need a financial advisor!"

And so when interest rates rose and slowed that down, that sort of activity in the aggregate, like we can see it in overall slowdown of new client growth. So to me, just interesting to see, right? All these questions of yeah, just like we had so many years of members having huge growth rates year after year, like something somewhere out there has to mean there's a worse year than others. So just interesting to know, like turns out interest rate sensitivity and just like a slowdown of business liquidity events is what at least brings some relative slowdown to growth.

Alan Moore: Which is helpful for advisors who are building subscription based businesses, doing fee for service planning to know; especially as you see interest rates continue to go up, interest rate volatility, and sort of the impact that you can start to predict that it's going to have on your business.

Michael Kitces: And again, I look at that relative to the industry overall. This is true in pretty much any model, any segment you serve. Now, like, different models get hit by by different things. Like, if you live in the AUM model, you just kind of know as an owner, like, I'm going to have some pretty sweet margins except two out of every ten years when I get no money out of my business.

Like, I just get a goose egg pretty much two out of ten years whenever the bear market comes through and ripples through and all your staff and expenses are still there and your revenue gets clocked and it just obliterates your bottom line. That's part of why advisory firms on the AUM model have historically run at these, like, 25 ish percent margins because that's how much buffer you need in one or two horrible years.

Otherwise, you literally go upside down and your revenue is lower than your expenses. And suddenly you have to come out of pocket to make payroll, which pretty much no business owner wants to do once they've gotten to profitability in the first place. So, you know, AUM models get, get slammed that way.

Turns out, at least for what we're seeing now, like subscription models, or at least where the clientele that subscription models are focusing into seems to be a little bit more sensitive to interest rates and, and, you know, interest rates go in cycles as markets do. You know, IPO cycles in general rotate through every 10 years.

So, you know, this too shall pass, I think in firms that are seeing those slowdowns in the same way that you get through bear markets in the AUM model. But, you know, market cycles are a thing and subscription models to me just like, it's not immune. It just turns out it gets hit in different environments.

Alan Moore: And if this was a bad year then it speaks very well for the future of these firms.

Michael Kitces: Yeah. I mean, I... One of the things that I like to look at more broadly is, you know, there are some other industry benchmarking studies out there. Investment News does a pretty good one with Ensemble Practice, Philip Pallaviv's team, who actually helps to produce our study as well at XYPN.

And then Schwab actually does what now I think is technically the largest benchmarking study out there, cause they have a bajillion firms now with the with the merger. And they, they do internal benchmarking studies out to the advisors on the Schwab platform which is kind of almost by definition, overwhelmingly, almost all AUM firms. And your Schwab's client growth rate last year was six.

Alan Moore: And that's really been the average.

Michael Kitces: That was a good year, because the five year compound growth rate was 5.1 . Last year, at least, they got to 6. So, I do find it striking at the same end, like, yeah, you look at the slowdown, like, and I'll call it this relative slowdown that we saw in growth rate. From the market cycles on a lot of XYPN member firms, but relative to AUM firms. Like, XYPN firms are still doing only 3x the growth rate of the average AUM firm instead of the 5x growth rates that it's been for the preceding five years cumulatively.

Alan Moore: Which really also speaks to the concern that you know, folks in the industry have been expressing since we started almost 10 years ago. And that was will clients pay for financial planning. Does it, will they just pay a fee for financial planning or is the only way to charge them going to be a commission or an AUM fee? And the answer is a resounding yes! There are way more consumers who are able to pay out of cashflow, out of income for financial planner than out of assets simply because just not enough Americans have enough assets saved for that to work. And we are, we continue to see the growth rate of XYPN members be exceptional when it comes to client growth.

Michael Kitces: And I mean, to me, that's still like the biggest underlying point to me of just looking at the, at the growth rates overall. Like, yes, I'm so thrilled to see so many of our members focus in niches and specializations. And we have some data that we'll show later that like, that really does accelerate your growth rates further. But I don't think it's as though like XYPN's got an average annual growth rate of client household of 29% and Schwab's average is 5% because we have niches and most AUM firms don't.

It's there's so much pent up demand for people that want to be served on a subscription model relative to how ridiculously difficult it is to find someone to be an AUM client that actually has money, it's liquid, available to invest and not one of the other, like 299,000 advisors who had gotten in front of them and gotten that money already.

Like, they're...

Alan Moore: It's just less competition for those clients.

Michael Kitces: It's hard to find unattached AUM clients at this point, right? To me, one of the reasons why you see so much merger and acquisition activity in the AUM model is AUM firms cannot find clients to grow with organically, so their organic growth rates are low single digits. So they're buying each other cause it's the only way to grow.

And we look within XYPN and the member network and growth rates like this, and right? Everyone's conversations like, "I've got capacity problems, I've got scaling problems, like my problem is I'm getting clients at too fast of a clip to handle this". And if you just look in the aggregate of 5% growth rates for AUM firms, like think about that relative to how many clients you actually have in your firm. It's like, a lot of firms, their good growth year is like, we got three this year.

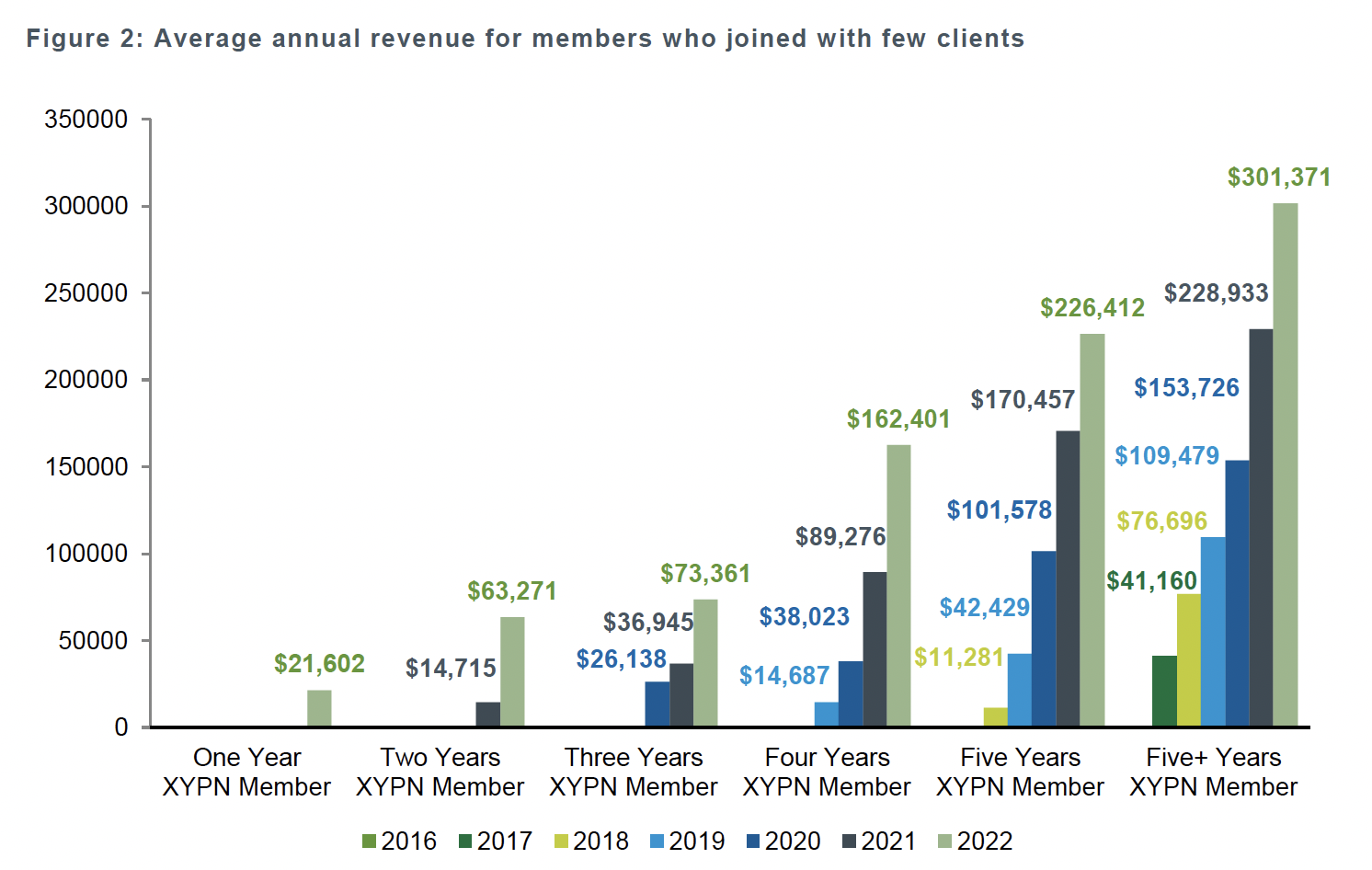

Alan Moore: Yeah, we have a lot of members that are getting three in a month, so yeah. All right, so we're going to move to the next chart, which talks about the average annual revenue for members over time when they've joined XYPN with few to no clients. And so the reason we look at this is because we want to be realistic with our firms that are starting from scratch.

They're not able to bring clients with them. Maybe they're a career changer, starting a business, you know, doesn't want to go be a W2 employee in our industry. Like they want to start their own firm. We want to be sure that we're being realistic and setting proper expectations for what can you expect from year one, year two, year three?

What does it look like long term? And this chart has tons of data on it. So again, you know, if you're listening to this...

Michael Kitces: We've been making this chart for several years and then we keep adding more data with each new year. I'm like, we might have to reformulate the chart a little. It's getting a little busy!

Alan Moore: But if you're listening to this recording, you know again, XYPlanningNetwork.com/373 and you'll be able to look at these charts. But basically what it sort of, what it shows is the progression of our members and sort of their revenue over time. And really, you know, what it speaks to is just how hard those early years are. And really, you know, like we've been saying for a long time that from year three to year four, sort of the end of your 36 months in business is really the tipping point for, you know, when we see advisory firms really open up the floodgates.

Michael Kitces: Yeah. I mean, this is an interesting charge as we, we've been producing this for a long time and it really changes remarkably little. from year to year as we keep repeating the benchmarking survey. Essentially what it says is, look, the first year is just horrifically bad for everyone. Most advisors get something like $10,000-$20,000 of gross revenue.

Your net is almost certainly in the red. Like gross revenue, maybe you're getting $10,000 or $20,000. By year two, you're at about $50,000, give or take a little. By year three, it goes to a little over $80,000. And you'll notice you kind of think about that progression like $20,000, $50,000, $80,000, like it's fairly linear.

You're just sort of like, I mean, basically you're grinding out about $30,000ish worth of annual new revenue each year. The first year you're lower because you only get a partial year, like first few months I don't have anyone yet, then I signed my first client, I only get six months of revenue in the first year because I signed them halfway through the year.

Basically like we're signing this neighborhood of like $30,000 of new client revenue each year. We get a partial year the first year, then we add another group of them that we get to bill for the whole year. Then we add another group of them that we get to bill for the whole year. And just a sort of thing that it's like, it's very hand to hand combat. Like one client at a time, one prospect at a time, anybody I can get in front of to try to get some business.

And then there's this turn you said on, and so we see this progression. Like, it's about $20,000 in year one, it's about $50,000 in year two, it's about $80,000 in year three, and then it's $160,000 in year four. Which basically means you add as much revenue in year four as you did in the first three cumulatively combined.

And we've seen this for a long time, I like, I just, having grown multiple businesses. I did an article about this back like, I want to say like 2015 or 2016 on the blog of, "Why it takes three years before your business gets going" and like, it's true. I mean, even I've done it in other, other segments of the world.

It, it's always three years. It's kind of aggravating. A little frustrating. You're in year four going like, where were you? Where were you in year two? And I could have really used your revenue. But I think there's just this phenomenon of it takes a certain amount of time. Raise the business, saying the businesses like, you know, you have to be known, liked, and trusted to, for people to want to do business with you. And just...

It takes time to be known, and liked, and trusted, right? In the purest sense, like you're going out into whatever community or specialization or niche or local networking thing you're doing, right? The first year you're just showing up a bunch of people are figuring out who you are. The second year you get more involved in whatever that organization, community, networking thing is.

You get to know some people like, alright, I kind of like this person, getting to know them. Then you show up for the third year and they're like, It's still showing up! Like, I guess they're, they're legit. Like, this must be, this must be for real. They're, they're still hanging around, like, I, I think I trust, like, this, this person's really like an advisor who's here to stay.

And then next year I do business with you. I'm like, it took three years to get through just this known, liked, trusted sequence and... But just as we find there's not a lot you can do to make that faster, that's why we'd say like, have your runway, have your, have your financial transition plan, have your reserves about how you're going to navigate through that. Cause it's just, it's hard to accelerate that curve.

Some people get there faster cause they're career changing from a prior industry where they already had friends and colleagues who trust them or like they're breaking away from another firm. But they've already been in the industry for a while, right? If you've already set some of those roots, in whatever you're going to focus on, you may get there a little faster cause you're getting to build on the past. But if you're really starting from scratch?

Just, this is the pattern we see over and over and over and over again.

Alan Moore: And obviously with all data, this is an average. Some folks are going to be above, some folks are going to be below these numbers. And it's not intended to create you know, any like, Oh no, I'm failing because I'm not hitting this number.

It's really just to show a benchmark for on average, how are XYPN members growing their practices, growing revenues you know, across the country, because this is going to have folks from Iowa and California in it. And so we're going to have different costs of living, different, you know, different metrics there that are all sort of getting rolled into this data.

But I, I think this is really telling and again, continues to reiterate this message of you know, if anytime an advisor calls and says, all right, I need to make a hundred thousand dollars in the first year or even the second year for this to work. It's like, then go get clients and be able to transition over with a book of business because it is very, very rare that anyone's going to start from scratch and do that level of revenue.

Cause in their first year, cause as you said, you know, we only get. Get half the year for some of those clients. Even if you had $100,000 of run rate revenue looking out over the next 12 months, you would not have gotten that in your first 12 months. But to be prepared financially for, you know, for the early years, which can be a slog, you know, in the end, it's really not that expensive to run and operate an RIA.

You know, you can be pretty lean. But you do have to ensure that your personal expenses are covered, that you can cut back savings and that sort of thing for a couple of years while you're getting going, invest in the business. But you still got to pay the mortgage, still got to pay the car loan, still got to pay for daycare, whatever the things are to ensure that, that you're able to make it.

So, you know, I, I would encourage listeners to use this data as a sort of a roadmap for what you can expect and sort of goals to hit. Again, you may be a little higher than these numbers, you may be a little lower but it gives a nice benchmark to, to look at. All right, moving on to our third chart, you know, really from day one, we've been talking about niches.

You know, I, I was reminded this week Kristen Herrod is here at the XYPN live conference. And I was reminded that I think she's the first one who introduced me to the concept of a niche. She was just a mark, a marketing genius for, and it was in corporate marketing for a long time and then started her own firm planning planning for parents.

And I believe it was at planningforparents. com. And I just remember, you know, she would say, I only work with families in the San Francisco area that have a kid under five and advisors would be like, Oh my goodness, like there's not enough clients out there. And she's like, are you kidding me? You know how many families there are where the kid under five and, and you know, that was probably, you know, 10, 12 years ago now.

But, you know, that was really sort of this first introduction of like, wow, you can really grow a really successful business focusing on a really, what would be considered a narrow niche of clients. And so from really from day one, we've been sort of beating this drum to say you know, in order to build a successful business, in order to, to be able to, to I would say long term scale be able to compete in the industry with larger firms that have more resources, bigger marketing budgets, fancier office space.

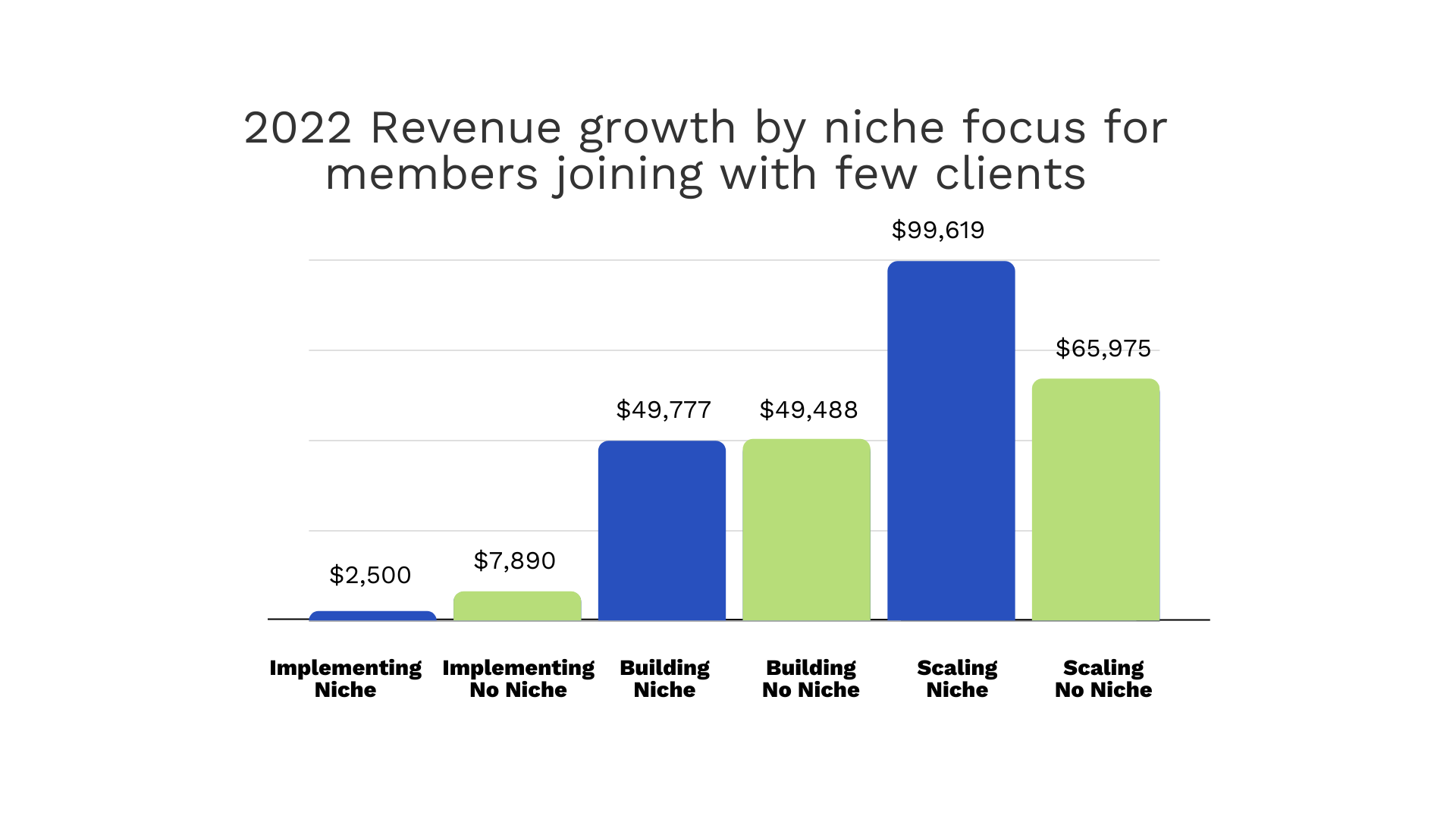

You've got to get focused. And so this chart shows the revenue growth by whether or not a firm has a niche or not in sort of the different phase of their business. And so we break this chart breaks it out into three phases. The implementing phase, which is basically I believe zero to. 20 clients the building phase, which starts at 20 clients and goes up to 75 clients or about 150,000 in revenue.

And then the scaling phase with at what point the firm has hit 75 client households and or 150,000 in revenue. And what this chart shows is that you know, in the early. So, in the implementing phase and the building phase, there's not a lot of difference between in terms of revenue growth by niche firm or not.

It's neither holding you back nor is it accelerating your growth in the early months, early year or two. It's really interesting in the scaling phase that all of a sudden, again, sort of the floodgates open and we see these firms growing significantly faster. And so it's, and so this is new revenue for the year, correct?

Michael Kitces: Correct. Yeah, the, the... But what we want to look at here is specifically as firms are across different stages, just how, dollar for dollar, like how much raw dollars of new revenue did you add over the past 12 months, depending on what firm stage you're in, right, because obviously at some point larger firms can add a little bit more revenue a little faster cause you're, you're larger, you may have more people, you can get more client referrals cause you literally have more clients to refer. So we wanted to segment them out by what stage they're in cause there is just a tendency of the larger your firm, the more you can grow cause the more client base you have to to build from.

But also to specifically segment out like just at firms that have focused in the niches versus those that have not. And can we see differences in, in what their growth patterns look like?

Alan Moore: And it makes a lot of sense that in the early days, you know, when you do have a niche, you're going to have friends and family and folks from outside that niche market reaching out to you saying, Hey, you know, do you provide services to me?

And if you're turning that business away, clearly that's going to impact those early years of revenue. But it really is about laying the foundation to build on then. Because if you have a lot of clients from outside your niche, eventually you hit this point of max capacity. You have your 75, 100 clients, whatever the number is, and you, but you know, you've given up half the seats on the bus to clients that you don't really want to be working with long term.

So now you got to go graduate, quote unquote those clients, move them to a different advisor or whatever the, however you, you end up managing that transition. And it's a really painful process. And I think what you see. Is, you know, once you hit sort of the scaling phase where capacity becomes a challenge, these firms that have a niche focus have really, it's a lot easier to streamline your processes when you are focused on a single client single client type or single client challenge that sort of defines your niche versus trying to be all things to all people and doing a little bit of this and a little bit of that, and you're switching from doing a social security analysis to a student loan analysis in the same day, you're gonna be a lot less efficient.

Michael Kitces: Yeah. The... the phenomenon I find that because growth is so brutal for everyone in the early years and because of this phenomenon that it takes three years to be known, liked, and trusted just as we sort of show in, in the, in the charts here through implementing and building phases There's basically no material difference between whether you're growing in a niche or not, right?

Just like, when you're in sort of this hand to hand combat phase, like, I'm just trying to slog it out one client at a time. Like, a new client's a new client's a new client. I don't have enough clients to fill my time. I would like more clients so that I can actually get paid for my time. So any client I can get fills my time and lets me get paid for my time and feels like a positive step forward.

And, and, because it takes so long for that known, like, trusted effect to kick in, You basically can't see much difference for the better part of the first two or three years. Then you get to the other end of that and just what we see you know, the, what, what the chart shows is when you get out to the other side, suddenly the firms that have built in the niche specializations are adding revenue at basically a 50 percent higher rate, like you're about 66, 000 a year versus 99, 000 a year.

You're suddenly adding revenue at a 50 percent higher rate because Either you spent those three years just like churning it out one client at a time and growing linearly or you were setting a foundation as something that has focus and you come out the other end growing exponentially. And to me in the purest sense like that's the difference that you see on these is it basically doesn't change your trajectory much in the first three years.

The question is when you get to year four, is year four just another grinding year like year three, you just get a couple more client referrals on top. Or as year four, I'm growing exponential momentum because now I'm actually known in my community of whatever the thing that I was trying to get known for.

And suddenly people are just sending me business from all sorts of directions. Even like people I've never worked with send me business because they know that that's my thing and they met a person who needs help with the thing and they sent them to me. And you know, most of us remember pretty clearly, like the first time I get a referral from a client.

And the first time I get a referral from someone I had never actually worked with in the first place. And... That second part comes a lot faster and more powerfully we find with, with niches. Just you literally get known for a thing and people are like, Oh my gosh, I know a person that helps with the exact problem you're dealing with.

And those, and those, that additional layer of referral growth starts to come.

Alan Moore: And we do see a lot of cross referrals between XYPN member firms when they do have a clearly defined niche. That means they're going to have folks who are reaching out potentially that, that are not in that niche. And they want, you know,

most of us got into this business because we wanted to help people. We didn't want to turn people away. We wanted to be sure they ended up with a good advisor, a fiduciary advisor. We didn't want them to sort of send them out into the wilderness and end up with a, with someone just selling them a product.

And so the ability to then connect those prospective clients with another advisor that's going to be a good fit for them, that, that provide services for them. It's just, it's, it's so much easier when you have a clearly defined niche versus when you're sort of, you know, I work with individuals, families, business owners, women and trusts.

You know, it's like, okay, well, so who am I supposed to send you? Like, I guess everybody? Like, but I've got seven, you know, we have almost 1, 800 members. Which one am I supposed to say, you know, is going to get that referral? And so if you're really clear on, you know, we work with, you know, folks with equity comp challenges, or we work with small business owners. Or, um, you know, there, there's just a whole range of things that you know, we have members that works with online sex workers.

We have members that works with Chick fil A franchise operators. They've just got a whole slew of different things that, that, um, of different niches that have been featured on the podcast over the years and just, it makes it so much, you, you would just become so much more referable when you have a niche that you can clearly define and that others can then clearly, they really understand what it is that you do and who you do it for.

Michael Kitces: Yeah. I, you know, to me it's, so on the one hand this is why. Like, you look at anyone that's scaling successfully in the niche, and I have literally never heard anyone say, "I niched too soon."

Alan Moore: Or too narrow, even.

Michael Kitces: Or, yeah, too narrow even. I have heard many, many, many, many, many, many, many people say, "I wish I'd done this sooner. I wish I'd focused it sooner." Now the one thing I, I would attach to this. To me there, there is a misconception I find around sort of niches in the phenomenon of trying to niche early, which is this fear like, well, I'm afraid to niche because I just need any revenue I can get from anyone that talks to me.

If someone talks to you and they want to give you their life savings, take their money. It's okay. No one's saying you can't do that. You're saying don't market to them. If I go out there and say, I'm the leading expert in the area in recent divorcees and someone just comes up to me like, I heard you're a great advisor, will you work with me?

Like, sure! I'm not marketing to you. I'm not trying to reach out to you. I'm not going to go to any networking meetings to meet you, I'm not going to have any marketing materials for you, my website's not going to speak to you. But if you know I've been an advisor for a long time and you would like to give me your life savings and have, and pay me to give you a financial advice, I, yes okay, that's fine, you can do that. The point is not "You're not allowed to" or not going to take people outside your niche. The point is you will spend zero minutes marketing to get them. Because you're gonna spend a hundred percent of your minutes built going into that focused area because the more time you spend there, the faster you can move that known, like, trusted curve. Otherwise, it's not even, you're not gonna be there in three years, it's gonna take you four years or five years or seven years to get there because you... If you literally don't show up as much, you're not going to build the relationships there as quickly. So the point to this is not, you don't take anyone outside your, your niche. If you're, if you're going to niche early, the point is you don't spend any time marketing and trying to grow outside your niche.

You can take what comes. The only asterisk to that, though, that I think Alan, you did highlight well, is... When firms get specialized and you get several years out and now your problem is not I've got all this time and I don't have clients. Now your problem is I've got all these clients and I don't have much time, right?

You start feeling capacity constraints and you start feeling the, the, the pain of scaling. Now you do get to a point often where you start to realize those non niche, non ideal clients, they take a lot more time. Because they don't fit your systems and processes, cause they need like different things that don't fit your standard offering, and often they're paying you less.

Because when we have a focused, specialized offering, we can often command like a good premium price for a premium quality offering. You're not a premium offering to your client that doesn't fit your specialization. You're just like an advisor they paid off the street to do something. And so the, you can quickly get to a point where your non niche clients have, are, take the most work and pay you the least for your time.

And become a problem from that problem, air quotes, a problem from that perspective. Which means the only warning I really give to people, if you are going to take clients outside of your niche early on, is you have to be prepared to graduate them when the time comes. Not now, not like you need the revenue and want the revenue, take the revenue, that's fine.

But when you hit capacity and now suddenly your choice is- I can work extra hours on evening and weekends, I can hire someone who's sole job is to do the work with the clients I don't want to, like, go of who pay me the least, which also means I'm going to lose money on the person, or I can just fix my practice and realize that a client that's not profitable for me is probably not one I should be serving.

If you're not ready to deal with that when the time comes, that's when problems start to crop up. So it's not about saying no to the non niche clients now, but it is recognizing that if you take non niche clients now, just you need to be mentally prepared that there will be a point where you're probably going to need to graduate them.

To continue your focus or your business is going to get less efficient and less profitable.

Alan Moore: And I will say in the end, you've got to pay the bills, but if you have the choice, my encouragement is do not take clients from outside of your niche. The firms that we, that I see be the most successful have a process that is so geared. Their, their, their entire planning process, the entire client experience, all of their marketing is so geared towards their niche market that anyone outside of their niche would just be uncomfortable going through the process. Like it just wouldn't work for them. And, and really I, that's just how we see firms continue to, to differentiate in this marketplace. When, you know, when zip code and, and who has the closest office to, you know, to my house is no longer sort of the differentiator for these firms, it really does help to be so clear. And it's not just saying on your website, Oh, well I work with this particular profession. It's that literally your fee structure, your service model, the entire experience, the technology you're selecting, really does show that that's who you work with.

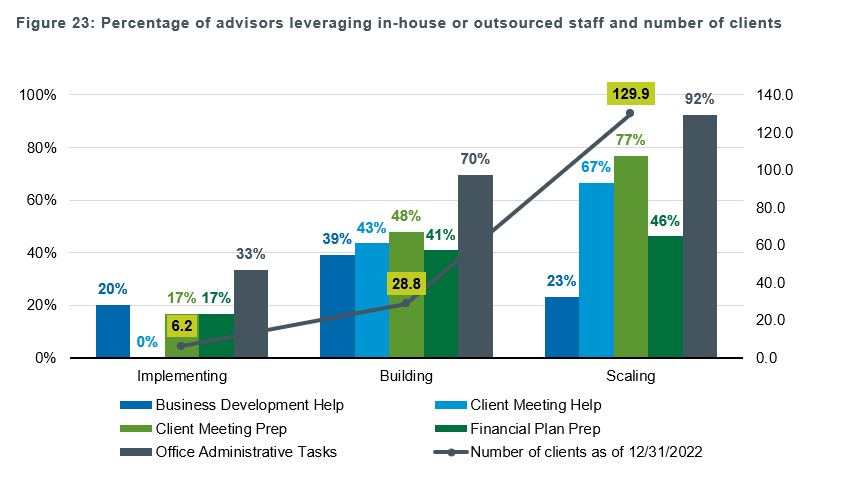

So moving to our fourth of five charts so the fourth chart also has a lot of data points on it. So I would encourage you to pull this up if you're listening to it on on XYPN Radio. But this chart shows the percentage of advisors that are leveraging basically staff either in source or outsource, whether they're hiring or outsourcing to a platform.

And sort of the different phases of their business as well as it also overlays the number of clients. So you can see here in the implementing phase, the average firm has 6.2 clients, which, you know, these are by definition sort of where you're at in the phase based on number of clients. Cause the building phase, then you have just shy of 29 clients.

And then scaling has an average of 130 clients. And what this is showing are what areas of the business firms are starting to use outsource or in source providers. They're hiring help in order to hand off some of the tasks associated with these various areas.

So the five that we measured were business development help, so getting new clients, client meeting preparation, office administrative tasks, client meeting help and I'm assuming that's like actually in the client meeting and providing assistance there, and then financial planning prep, more of your para-planner type service.

So, it makes sense when you look at this chart. Just in general, firms are starting to outsource more and more over time. The one that does drop though, it's kind of interesting, is business development help. There are more in the earlier phase, which makes sense. There's more in the earlier phase that are outsourcing business development. Versus those who are a little bit more established and maybe have more clients.

Michael Kitces: Once you can delegate more, you've got more time to go out and drive some of the business development yourself.

Alan Moore: So what do you see when you're, you're looking at this chart and you're seeing, you know, the amount of, I I, I'm actually amazed at the percentage of folks who are in the implementing and even building phase that are outsourcing in some capacity.

What we're finding is that, I mean, this tells me XYPN members are outsourcing really early. Maybe, I don't know if it's too early, but they're definitely doing it early.

Michael Kitces: So, so there were sort of two things to me that really, that really jump out in the charts here. So like one, one directly and one implied.

First, just directly, when we look at where hiring and outsourcing is happening most and fastest, it's like, simply put, it's administrative work. It's not planning work, right? Like we are overwhelmingly outsourcing or getting support for administrative tasks, meeting prep. And, right, and sort of like paperwork-y and documentation-y related things, whereas areas like financial planning prep is, is much, much lower, is a significant laggard on this.

So, right, so it sort of makes sense to me intuitively, right? If you think in the, in the classic, like, you know, focus on your highest and best use and delegate the things that are, that are the lowest dollar amount, right, just sort of mathematically. Like I can admit, I can delegate administrative work at a lower cost than planning expertise work at a lower cost than like leading clients.

So that's what I tend to delegate first. And, and we, we see that pretty clearly in the rise of delegation of administrative. The, the thing that strikes me about this though, just when I, I, I look at it at member firms and we, we, we didn't directly, measure this in the benchmarking study, but I, I know it crops up and I'm seeing it happen a lot across member firms.

A lot of members, their first hire is not an administrative person.

Alan Moore: It's an advisor.

Michael Kitces: It's an advisor. It's an associate advisor. But then when we look at what are you giving the associate advisor to do, you're, we're giving them mostly administrative work and maybe a tiny bit of planning stuff. So we like justify and rationalize it's, it is an associate planner hire. But like, just look, I, I love creating opportunities for more advisors, some of whom may be listening to the podcast and hopefully are looking for these job opportunities, but I have to like put on my business owner hat first and foremost and, and, and start asking the question, like, "Are firms hiring associate advisors too quickly at just what ultimately is a higher price point", right?

It costs more to get a good high quality associate advisor than to get a good high quality administrative team member. Are, are we hiring associate advisors too early? And then paying them to do administrative work, which frankly at that point is not, not good for the firm. You're spending more on, on staff than you need to for the tasks that get done.

And ultimately I would argue is not even the most ideal for associate advisors because most of us when we're coming in at that stage of our career are kind of looking for like a planning job, not a mostly administrative work that occasionally gets a little bit of planning stuff job. So this does to me raise, just raise questions about whether we're being a little bit too fast to hire associate advisors and a little bit too slow to hire administrative help. When I look overall, and we, we have some separate work on this that we've done with our Kitces research studies around advisor productivity, that when we look overall, the most, most common hiring path by a pretty large margin is the first hire is administrative.

And then the second hire is an associate advisor, the administrative hire just, you shed a whole bunch of stuff that you shouldn't be doing, often don't want to be doing. It frees up a bunch of your time, you get back 5, 10, 15 hours a week that you really have to spend cause now you have like 20, 30, 40 clients and it's taking more time.

You let go a bunch of those tasks that lets you get further with your own client base because you free up a bunch of other stuff so you can just do planning work, reviews, get new clients, and let go of a bunch of the rest. And that gets you further down the road and then say "Ok, now I'm at like, 60 clients, 70 clients." I've leveraged the heck out of myself with an operations person, but I really just need someone to help do more planning work and be able to actually field some client phone calls and inquiries and do more on that end. Now I need the associate advisor who will be really productive because they don't have to do administrative work because I've now had my admin person on for a year or two or three who's got those processes dialed in.

And so now even when I hire my associate advisor. I can get them focused on the planning work that's meaningful much more quickly and we can continue to grow faster. So I, there is a, like, it doesn't surprise me at all looking at this saying we mostly let go of administrative work first, it kind of makes sense in the classic delegation sense. But this, this does strike me because the tasks that being, that are being delegated does not match to what I see a lot of firms choosing as their hiring sequence.

Alan Moore: You know, Jerry, our EOS implementer here at XYPN he'll say, "Job titles just confuse people". And, and I, we do see this, you know Monique who runs XYPN Ops, formerly known as XYVA. She'll have advisors reach out and they'll say, "Oh, well, I'm looking for an outsource para-planner". And, you know, initially she would say, "Oh, well, sorry, that's not a service that we offer. We're, we're focused on administrative tasks". But one thing she has found is if she starts to ask, "Oh, well, tell me more about what it is that you're looking for that pair planner to do. Tell me about some of those tasks". When they go through the list, it's all administrative tasks. Really, they're trying to just hire someone who does data entry, does administrative work.

They're not looking for someone who actually will do plan analysis, make recommendations that get vetted then by the lead advisor. And so some of it too is just literally how we use some of these titles, like Associate Advisor and Para-Planner. What do we really mean? Would you put para-planner on the administrative side or the associated, or is, or is para-planner and associate advisor sort of synonymous?

Michael Kitces: That's an interesting question, just in sort of a, a titling thing. I, I would characterize it more on the planning side, right? And sort of the purest sense to me, para-planners are doing financial plan preparation. Like here's all the data, gather the data, get the data into the software. Start preparing the analyses, crunching the numbers, and then, like, bring me something to look at so we can figure out what the recommendations are.

They may not be fully formulating the recommendations and they're certainly not delivering them to the clients. I mean, sort of, like, the difference, the core difference between the para-planner and the associate advisor is the associate advisor's in the meeting, and the para-planner never goes into the meetings.

They're, they're just, air quotes, sitting in the back office in front of a computer doing planning work. So, associate advisors typically are part of the plan delivery process and typically will have more client communication interaction as well. Notably, then, in that context, one of the other things that we found from our research is that for most advisory firms who hire a para-planner, the para-planner is typically the sixth hire or the seventh.

Alan Moore: And that's differentiating between para-planner and associate advisor.

Michael Kitces: Correct.

Alan Moore: So, you said first hire is admin, second is associate.

Michael Kitces: First hire is admin, second hire is an associate advisor. Third hire is a service advisor to, to handle, um, like lead client responsibilities, right? Like, okay, I appreciate you're in the meet,... you're associate advisor, you're in the meetings, you're handling some basic client correspondence and interaction,. But like, I literally need someone who can manage the relationship so I never have to show up to that client again cause there's just too many clients.

Like I need to hand off the client. So service advisor is often fourth. Now you've basically got kind of an Angie Herber style diamond team structure. At this point, often firms are looking at another sort of administrative operations support person if they've got an investment function, a trader sometimes shows up here. But just like, I got three advisors, if I fill them to capacity my admin person is going to start getting busy and there's other stuff going on.

Then as the firm continues to grow... , next hire is often one more advisor. We start spinning up a new advisor team now, cause my kind of core diamond is getting crowded. And at this point, I have often four advisors in various capacities, increasingly focused on client service. They're doing all of this client work and there's just so many darn financial plans because I'm probably now north of 200 clients.

It's like, can we just have someone who's really good at sitting in front of a computer and doing all the planning tasks? Because at several hundred clients, I have enough planning tests that I can actually fill someone's day just sitting in front of a computer doing Right Capital things, or e-Money things, or Money Guide things.

But it takes a lot of clients to actually keep an advisor busy, a para-planner busy, only sitting in front of a computer doing that work. When firms are earlier on, we find it's very rare to actually find a para-planner. Because, like, if you get away from titles in the two job... you know, job tasks, actual functions, either they're doing more administrative work and they might be called a para-planner, but they're really more of a client service administrator.

Or, they're really sitting in client meetings and interacting with clients on communication and what I would characterize more as an associate advisor.

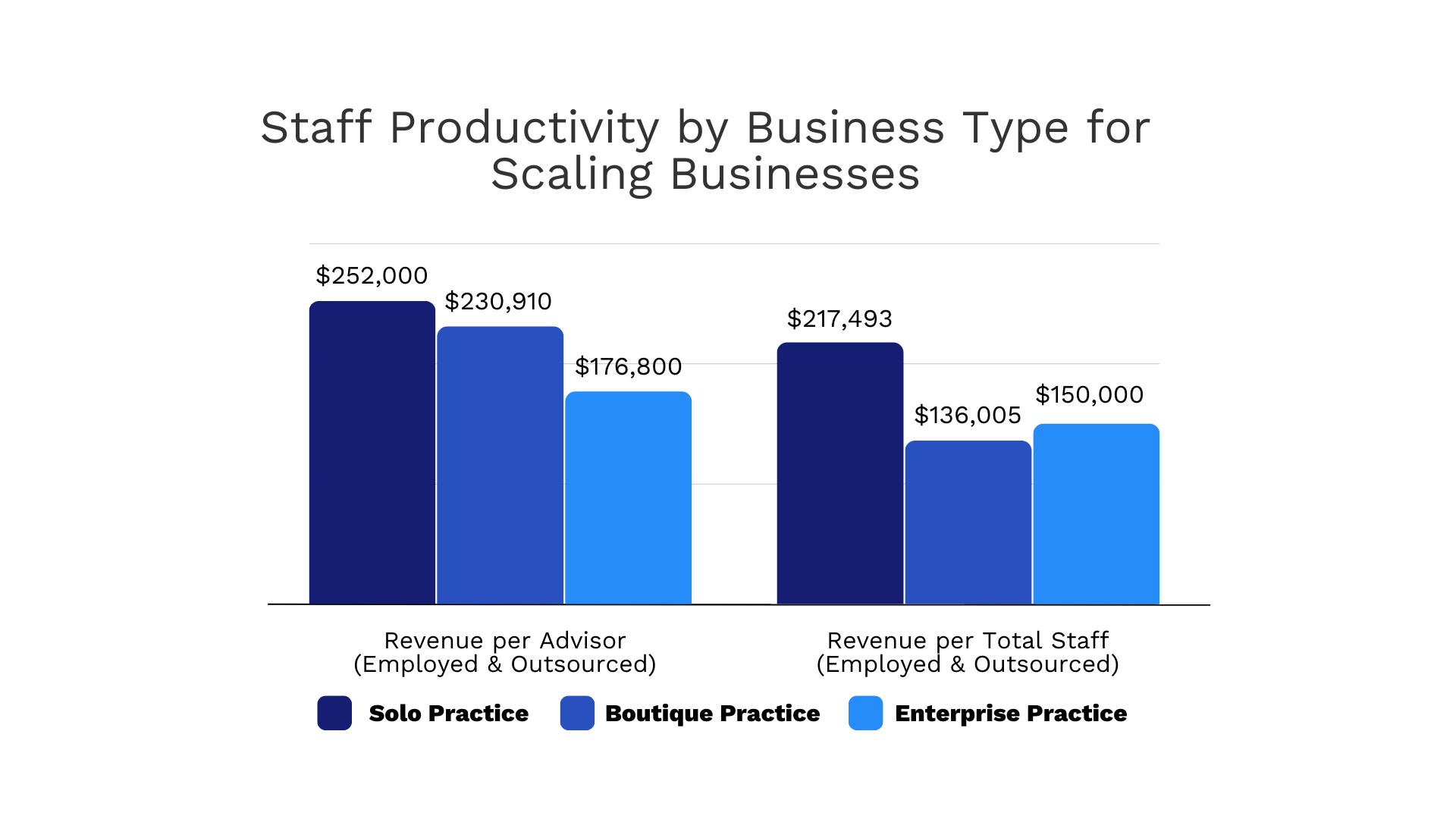

Alan Moore: Alright we're going to move to our final chart and this is staff productivity by business type. Now, these are measuring, basically, different types of firms between solo, boutique, and enterprise, which we've talked about on the podcast before but a solo firm is characterized as only having one advisor.

You may have support staff or admin staff, but there's one advisor. You have boutique, which is a multi advisor practice, and then you have enterprise, which is really, like 20 employees and above.

Do you remember the cutoff for this data set?

Michael Kitces: For this study, they didn't have to be as large on actual employee count, but they had to say their goal and commitment was building and scaling towards something that may be 20 plus people. As opposed to a lot of us there in the boutique realm.

And they're like, he sounds like a lot of like, "I'm just, I got three, I'm going to go to four, maybe in a few years I'll be five". And like, that's a comfortable pace. The folks that frame as enterprise tend to be very growth oriented and faster growth orients are like, "I'm going to build me a big firm".

These are the ones that if you were, they were AUM world, they would be saying like, "I'm building me a billion dollar firm here". Like that, that sort of mentality, except we don't usually talk about billion dollar firm in a fee for service context.

Alan Moore: And so what this chart is showing is basically gross revenue, top line revenue for the business divided by number of advisors.

So revenue per advisor, and then revenue per total staff, which then would include your administrative staff. These are two really important , KPIs, key performance indicators for any business. These are metrics that we track at all of our businesses and, and track it over time. Most of these are actually on a monthly basis to sort of see trends over time.

And so what we find, you know, what this data is showing is that on the revenue per advisor the solo practice is earning the most per advisor, which makes sense. If you really think about it, they're making about 250, I would say $252,000 per year for the solo. The boutique is making a little bit less per, per advisor, $230,000, and then the enterprise is making $177,000.

Now, do you see over time, you know, as the enterprise grows, obviously they're reinvesting, they're, you know, into the business, they're hiring ahead of the growth curve. Does this number tend to come up to match the solo practice or do enterprises just sort of forever earn less per advisor than the solo?

Michael Kitces: No. These numbers, this chart's supposed to go the other way. This is supposed to go up and to the right, as you, as you scale, not down and to the right. Now profit per client often gets lowered in, in larger scale enterprises, cause you've got more infrastructure, there's more stuff around you, your overhead allocation may be a little bit larger, but, so in the purest sense, these are measures of productivity.

These are measures of how much time... When the advisor does all the things that they do, how much revenue can that advisor support before I need another advisor because there's too much client task-y things to do. And one of the interesting things when you look at productivity measures in this context, it's like revenue per.

It, it's, I kind of call this the great equalizer. Like, I don't care what kind of fee model you have. Like, you can take revenue providers. I don't care whether you're on an AUM model. Whether you're on a fee for service model, whether you're doing advice only standalone plans, or some combination or mix of thereof.

In order for clients to pay a fee of X, you have to do some work. There's only so much work you can do before you run out of time. And so if clients are paying a fair value for the time that you're spending, and you fill all those hours doing the things you do for whatever the model is you do, you get to some amount of revenue.

That an advisor can support doing all the advisory things they're supposed to do to earn their revenue before they just sheerly run out of time at whatever clients are willing to pay and you say, "Well, it's time to hire another advisor". Right? That's, that's sort of like the natural capacity limitation.

If I've got a super slim scaled down model, I might do that because I've got like 200 clients. I meet with them once a year and I hardly talked to them in between cause we got a super simple scaled back model. Maybe that's because I'm like a multifamily office and I do this with six clients that I spend hours on every week all year long.

But whether you're a multifamily office that has six clients or you're a super scaled back model that has 200 clients. The 200 clients don't pay a lot of money per, the multi family office pays a lot of money per, and when you back into that from a revenue per advisor end, it's actually shocking how consistent the numbers tend to be across fee models, right?

At the end of the day, we are a service business, clients pay a certain amount of money for services rendered and this number kind of becomes the great equalizer. So the challenge from this perspective is... Classically, as advisory firms scale, one of the simplest ways to think about scaling an advisory firm is, as my team grows and my systems and processes improve, my advisor should be able to do more advisor stuff and less anything else.

Right? From the business owner end, there's often like, I want to get everything off my advisor's plate except client things because they are the most expensive employee in my firm. So frankly, I don't want them doing anything else except that. And what tends to occur in practice is as advisory firms scale up, revenue per advisor numbers typically rise. Because literally like you're pulling more off, you're pulling more off their plates.

They have more time to do nothing but be awesome for clients. And so by whatever means you do the awesome things and get paid by whatever your awesome fee model is. That number typically rises. So, not uncommon to see smaller advisory firms at about $250,000 of revenue per, per advisor. That's actually a very, very common number to see for firms as they're growing up towards about a million dollars of revenue.

Like $250,000 - $300,000 of revenue per advisor is not uncommon. So, like, I can be at $250,000 as a solo. By the time I have $500,000 of revenue, I've probably got two. By the time I'm $1,000,000 of revenue, I've probably got three and I'm about to hire my fourth as the, the number starts to lift. Because as we said earlier from the hiring sequence, like I've got one or two admin staff behind them now pulling things off their plates so I can get really, get my advisors more focused.

And I would note in this context, revenue per advisor in this is any advisor who is interacting with clients directly. So this is your lead advisor and your associate advisor that goes into this number. So ideally, firms start moving up and to the right. When you look at like the mega RIAs out there that are the like $5,000,000-$10,000,000 revenue firms, your proverbial billion dollar RIA.

You'll often see these revenue per advisor numbers get up to $500,000 or $600,000 of revenue per advisor. If you want to look at just like industry overall for context, if you pull out like the, the numbers from Merrill Lynch and Morgan Stanley, you can actually take their total revenue, divide by their total advisors, and even see what this is in large warehouse environments.

The answer there, about 1. 1 million of revenue per advisor. It turns out when you work with ultra wealthy folks, which is typically where wirehouses are focused, you just get paid more for your time. They do it in lots of different ways, but at the purest sense, like you work with ultra high net worth people, often they're paying you the equivalent of $600, $700, $800 an hour.

You bring that back to a revenue per advisor number, you end up with really big numbers. So to me, like the core concern on this is the firms that are growing are actually seeing their revenue per advisor drop when normally it should go up. In part, like, this is how I can tell from the study that we're hiring associate advisors and giving them administrative work to do. Because we're, we're getting numbers that look like what administrative staffing looks like, even as we're hiring advisors. But we're not actually getting better capacity, we're not lifting more revenue per advisor because they don't actually have time to do a lot of client things because they're doing a lot of non-client, non-advisor things.

Alan Moore: Well if you look at the chart, I mean, revenue per advisor in an enterprise firm being $177,000 revenue per total staff and an enterprise firm being $150,000, that means all but maybe half of a person are advisors.

Michael Kitces: Almost everybody in these enterprise firms are are advisors and, and just, I look at that and say, well, look, so there's two ways that you can end up being almost all advisors and almost all almost no administrative path staff. One is, you're hiring advisors and having them do everything, including administrative work and, and it's like, it's not a good staffing allocation. Like, just in the purest sense, you're, you're paying people a lot of dollars to do things that even they should be delegating.

I mean, you probably delegated so that that's why you hired them. But they're, they should be delegating it as well. You're paying people a level that's not commensurate to their skills, or you're giving them tasks that's not commensurate to what their capabilities actually are, right? And it's, it's sort of the proverbial, like, you've got a super awesome smart person and you're giving them intern work.

The second, the second way that you can get to this is you're one of those people that's super awesome at operations and systems. A few of us are just wired that way. I, I was talking to a member at XYPN LIVE, he is just shy of a million dollars in revenue, and it's literally him alone. He doesn't even have any admin staff, but he, like, his hobby is Zapier, and he's really good at it.

He has workflowed the bejesus out of everything. And the whole firm sings with his nearly million dollars of revenue and it's literally just him. That's arguably an extreme example. Almost no one gets a million dollars of revenue without admin support. But some of us are just, it happens to be how we're wired.

It's the gift that God gave us. We're really good at operations and admin and, and, or not, I mean, we're good at operations and systems. And we make the thing so darn efficient that we basically skip some of the admin hires and we just go straight to the associate advisor hire. But if that's your gift and where you are, you shouldn't need the associate advisor until later.

Which means if your gift is systems and operations and processes, you might have a, like a revenue per staff that's very similar to your revenue per advisor. Cause you have almost no op staff, but the numbers are fricking sky high because you just made like all of the administrative work automagically vanish through technology automation in your firm. So these numbers should be, your productivity numbers should be amazing because you made all of the work vanish. These numbers should just be like, we're not making the work vanish. We're failing to get sort of the operational leverage of a business by making sure that tasks are tiered to the person. That's best tied to those tasks.

Alan Moore: Well, Michael, we are up on time per usual, the, the red light starts flashing at us anytime we do a recording together. So you know for listeners, you can go download the Study. If you want to see all of the information again, you can also go to xyplanningnetwork.com/373. If you want to look at the graphs that we talked about specifically today, and this study is available to all of our members. So with that, Michael, thanks for joining me today on the pod for this episode and look forward to having you on next time.

Michael Kitces: Absolutely. Thank you.

Unlock behind-the-scenes content—subscribe now!

Featuring

Michael Kitces

Co-Founder, XYPN

Alan Moore

CEO & Co-Founder, XYPN

Share

XYPN’s 2024 Benchmarking Study Highlights LIVE

XYPN’s 2024 Benchmarking Study Highlights LIVE

Nov 15, 2024

XYPN’s 2022 Benchmarking Study Highlights

XYPN’s 2022 Benchmarking Study Highlights

Nov 2, 2022

XYPN’s 2021 Benchmarking Survey Results Review

XYPN’s 2021 Benchmarking Survey Results Review

May 19, 2021