These Related Stories

Share this

For the past three years, XYPN has partnered with The Ensemble Practice to produce a benchmarking survey that measures key information about XYPN members’ firms. The goal of the survey is to provide a roadmap for fee-only financial planning firms by showing how firms evolve from launch to running a business.

The survey focuses on revenue and expenses, client services, sources of clients/business, and pricing. Each piece of information is tracked year-over-year to show trends and provide fee-only financial planning firm owners with key metrics against which they can measure their own businesses.

The 2019 XYPN Benchmarking Survey was the most comprehensive report we have produced since introducing the survey three years ago. In addition to tracking XYPN member firm information year-over-year, we also started tracking information by business phase of the firm, allowing us to show how key firm metrics change as firms progress from launching, to building, to ultimately scaling their firms.

We recently highlighted five noteworthy trends from this year’s study. In this blog, we will further examine the fees XYPN firms are charging and how those fees have evolved.

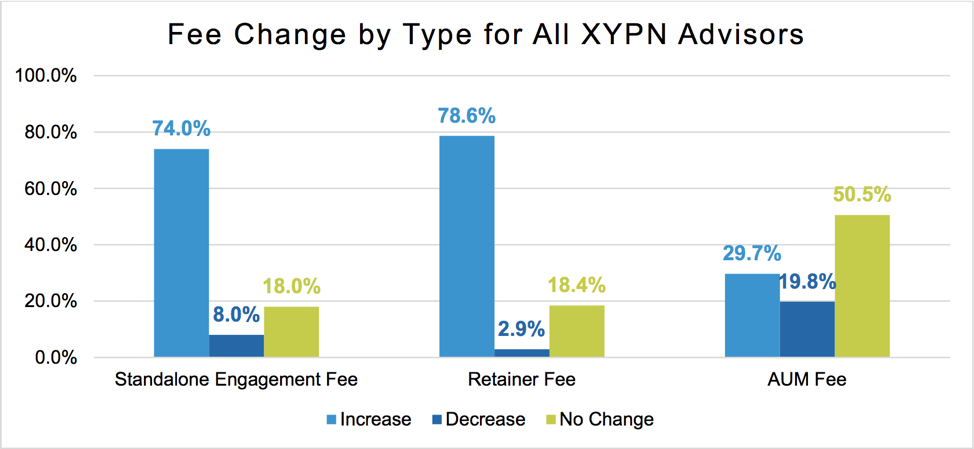

As we highlighted previously, approximately 75% of XYPN firms are continuing to increase their fees, specifically upfront planning and ongoing subscription fees.

We hear a lot about fee compression in the financial services industry and assume it applies to all fees advisors are charging.

However, fee compression is generally in reference to investment management fees due to lower cost options being made available to investors.

We have not seen this fee compression happening with fees paid by clients for planning and advice—we have actually seen these fees per client increasing.

With XYPN firms, this increase in planning and subscription fees can be attributed to a couple of factors.

First, when an advisor launches their firm, they are responsible for setting their fee structure and pricing the planning services they provide. In many cases, firm owners underprice the services they deliver.

This is often due to a combination of a lack of confidence to charge clients the appropriate amount (the amount the advisor’s time is truly worth) and not having a full understanding of the amount of time it actually takes to provide comprehensive financial planning.

The other factor contributing to the continued increase in planning fees is the ability for firm owners to communicate the value of planning and clients’ willingness to pay for their advice.

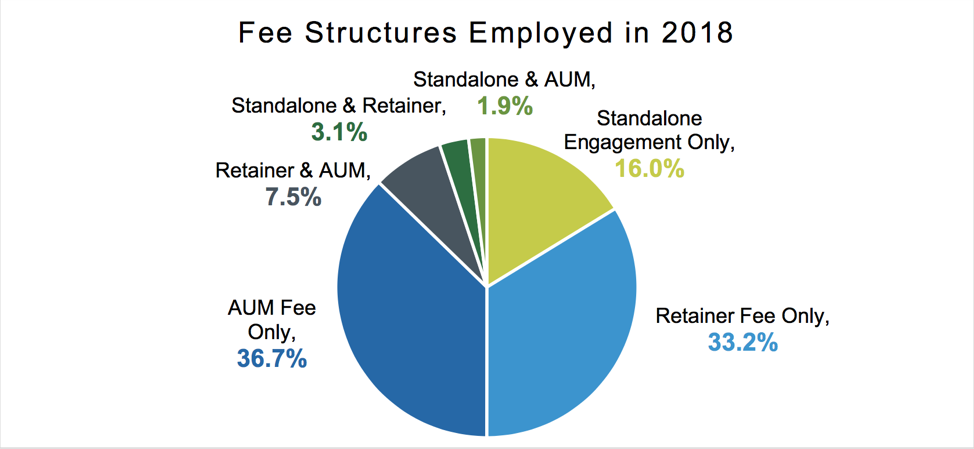

So, what are the fees XYPN firms are charging and how are they charging them? To answer these questions, let’s look at how XYPN firms charged fees in 2018.

The three most common ways firms charged fees are: upfront planning fees, ongoing retainer fees, and AUM, with retainer and AUM being the most commonly used.

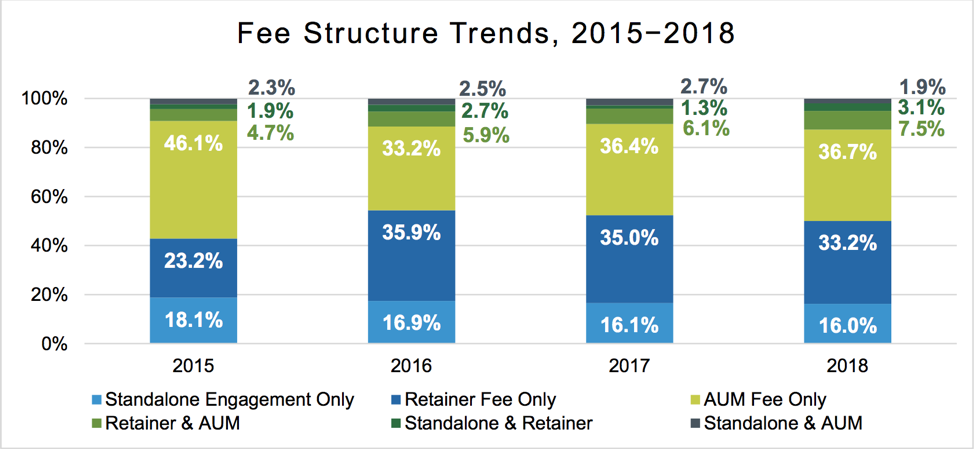

This has evolved over time and it's interesting to chart the type of fee structures used over the years at XYPN as firms have grown and retainer/subscription models have become more common.

In 2015, 46% of firms charged an AUM fee only while 23% charged an ongoing fee compared to 2018, when 37% charged an AUM fee and 33% charged an ongoing fee.

This shift will be an interesting trend to watch as AUM fees have stayed relatively flat while planning fees have increased. It’s likely more firms will shift towards the ongoing fee for planning versus an ongoing fee for AUM.

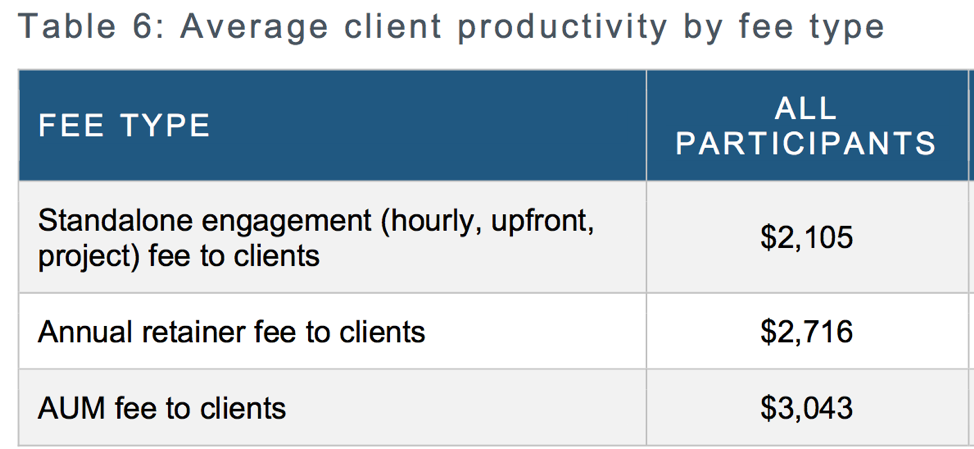

In the benchmarking survey, we asked for the highest fee, lowest fee, and most common fee advisors charge within each of the different fee types. Below is a breakdown of average annual fee per client for the three most common fee types:

While looking at the averages of advisor fees can be insightful, examining the median of each fee type provides more insight into the ranges XYPN members are charging.

For firms charging retainer/subscriptions fees, the median highest annual retainer fee is $3,000 while the median lowest annual retainer fee is $1,200. The median most common monthly fee is $200; this increases to $250 for firms that specialize with a niche.

For firms that charge an upfront planning fee, the median highest annual upfront planning fee is $1,500 while the median lowest annual upfront planning fee is $500. The median most common upfront planning fee is $1,200.

These numbers illustrate some of the ranges of fees firms are charging their clients under different fee structures. The data demonstrates firms that are able to clearly define their niche are able to charge more for ongoing planning and advice.

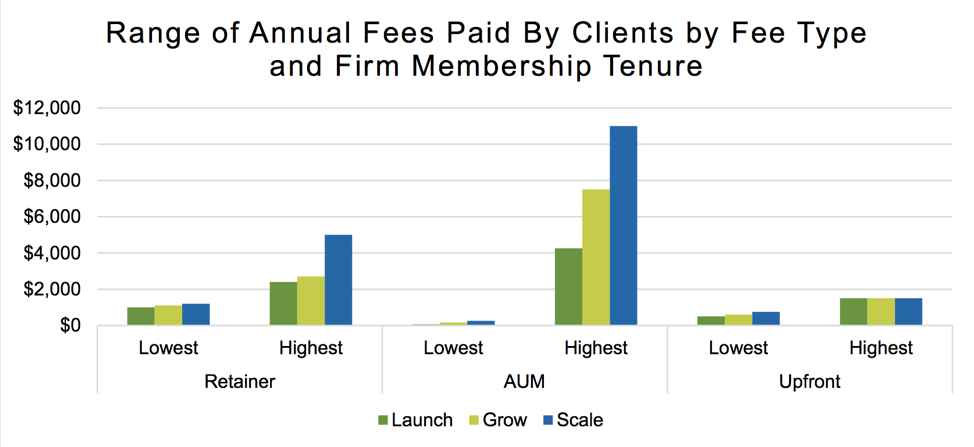

In 2019, we started to track fees by business phase with the goal of better understanding how firms that have just launched (within a year) charge clients as compared to firms that are growing (1-3 years) and firms that have started to scale (3+years) their businesses?

It’s no surprise that firms that are further along are able to charge more for their services. This can be attributed to many factors, namely these firms are better able to articulate their value to clients, along with the fact that as firms grow, firm owners are more accurately able to price the value of their services.

How to price planning services, whether upfront or ongoing, is one of the most common questions financial planning firm owners have when they launch their firms. As we have seen, most will underprice (undervalue) their services initially, and the majority will increase those fees in their first three years.

When determining your pricing as a firm owner, it's important to consider not only what your clients are able to pay for your planning services, but also the time it takes to deliver your services and the value you are providing your clients.

Don’t be afraid to update your pricing as your firm and service offerings grow—the value you provide your clients likely far exceeds the fee you charge them.

About the Author

As XYPN's Director of Advisor Success, Malcolm is tasked with doing just that—helping advisors succeed. After graduating from Gettysburg College with a B.A. in Management, Malcolm jumped straight into the financial services industry and never looked back. With a drive to help shape the future of financial planning and a passion for bringing financial advice to the next generation of clients, he has a lot in common with the advisors in the Network.

Share this

Subscribe by email

Top 5 Growth Hacks from XYPN's 2024 Annual Benchmarking Study

Top 5 Growth Hacks from XYPN's 2024 Annual Benchmarking Study

Dec 4, 2024

8 min read

5 Top Growth Takeaways from XYPN's 2023 Annual Benchmarking Study

5 Top Growth Takeaways from XYPN's 2023 Annual Benchmarking Study

Nov 6, 2023

3 min read

5 Noteworthy Trends from XYPN's Annual Benchmarking Survey