Share this

5.5 MIN READ

2020 was an interesting year. That’s stating the obvious, but for investors it truly was interesting to see how investments performed throughout the year. While it’s always important to stay focused on what’s ahead, there’s value in recapping 2020 investment returns for investors before looking forward to 2021.

What Were the Best Performing Asset Classes in 2020?

After the S&P 500’s +31% gain in 2019, few people imagined the stock market would continue to power ahead. COVID tried to ruin the party in the Spring, sending the index down 35% from mid-February to the end of March. But things quickly recovered, and the market was making new highs just a few months later.

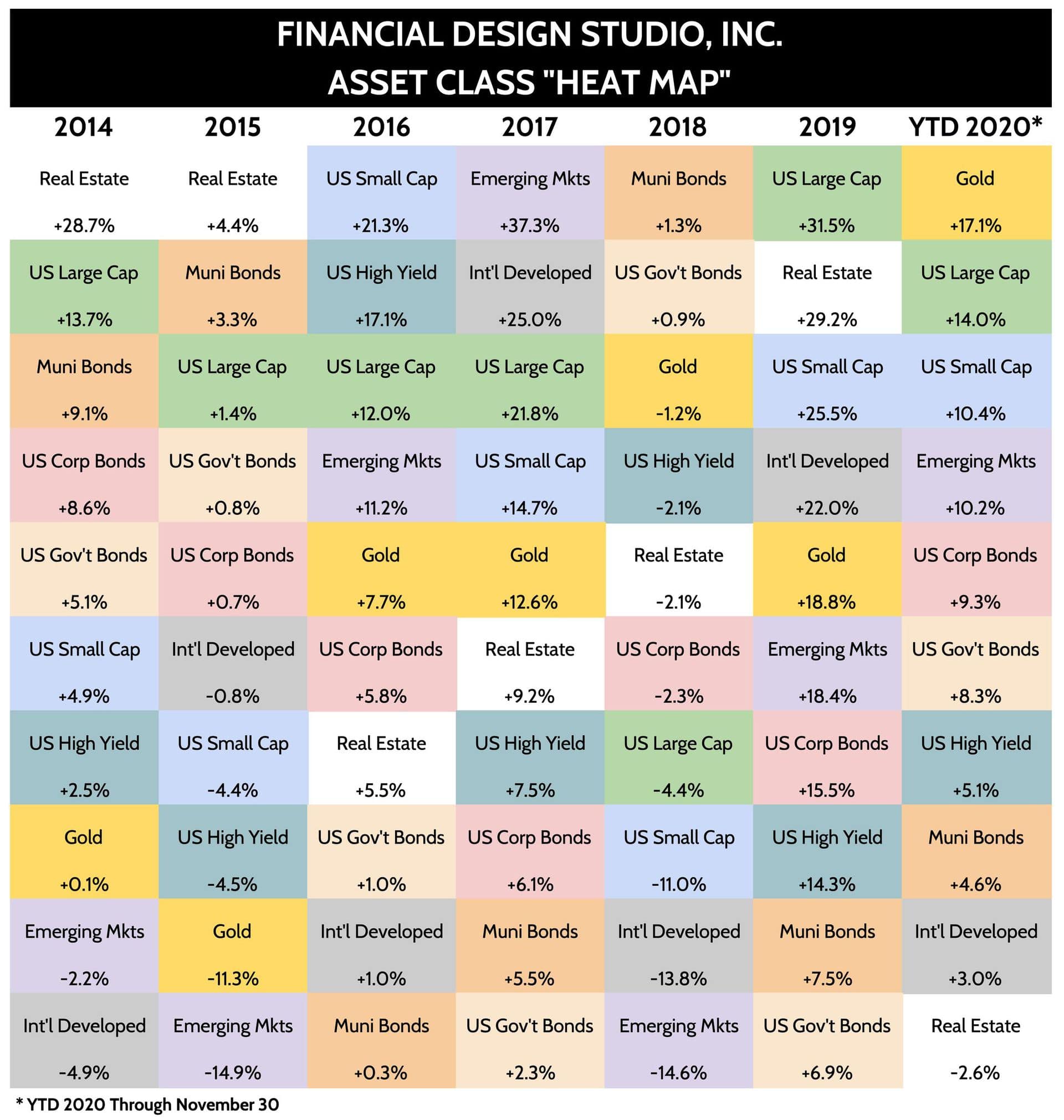

One of my favorite graphics is our FDS Heat Map. This ranks all the investment returns for the most important asset classes we look at. The data here shows YTD 2020 returns through November 30th.

So far in 2020 Gold has been the winner, up about 17%. That’s being driven by two things. One, the COVID-driven economic uncertainty has caused many investors to flock to the relative safety of gold. Second, investors are baking in a more aggressive fiscal policy and the potential launch of Modern Monetary Theory (MMT), which we’ve written about in previous Newsletters.

On the downside, Real Estate has been the only major asset class to generate negative returns in 2020. This is logical. With everyone working from home and states closing down business, there’s a lot of uncertainty about office properties and malls. 2021 could be interesting for Real Estate if a COVID vaccine is rolled out quickly, causing companies to call workers back to the office.

As We Continue Recapping 2020 Investment Returns Are Small Cap Stocks Ready to Outperform?

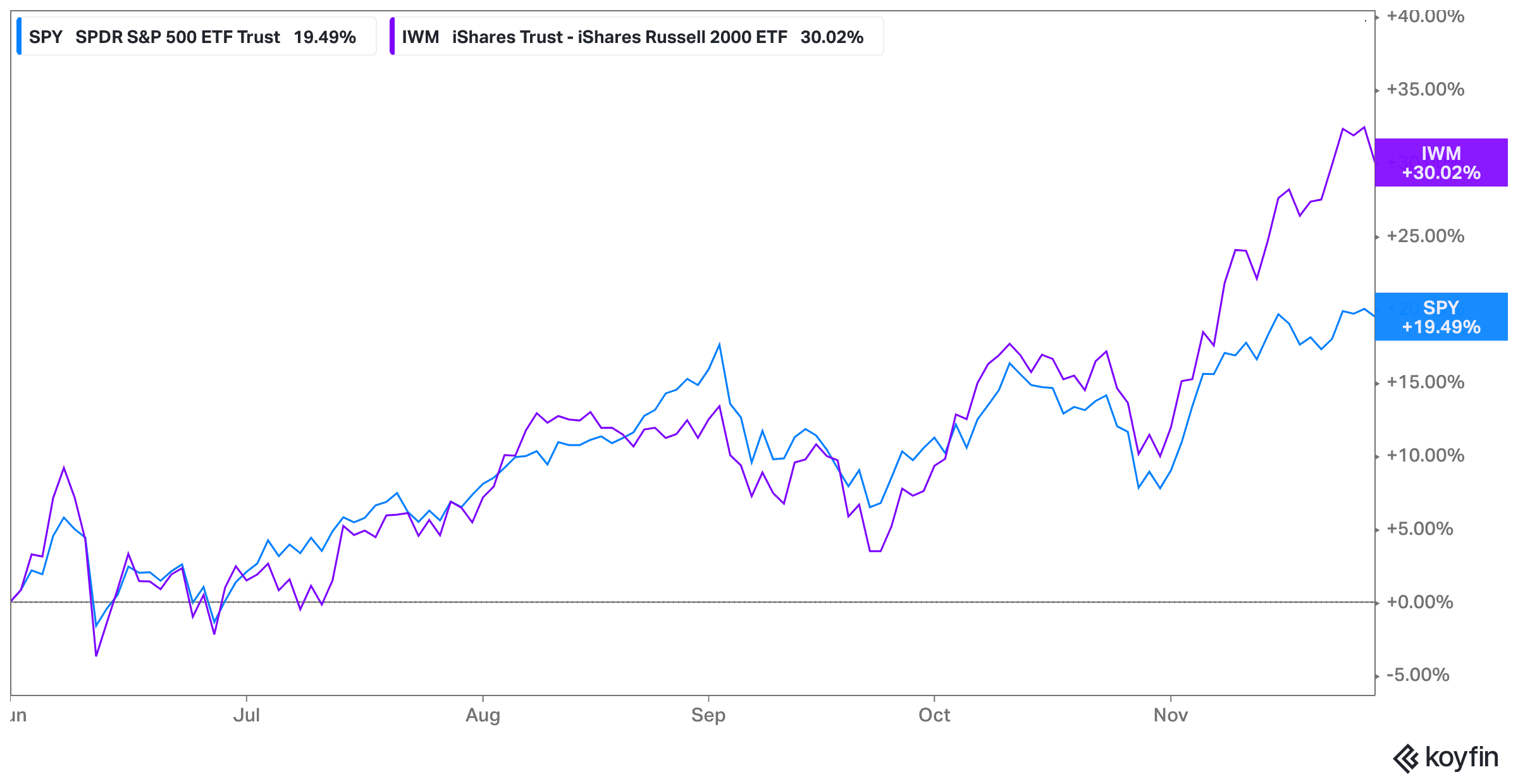

Our November 26, 2020 blog post highlighted the strong rebound in small cap stocks in November. As you can see in the table above, small caps have only beaten large cap stocks one time in the last seven years (2016).

The gap in performance has added up. Over the last seven years, large cap stocks are up an annualized +10.2% while small cap stocks are up only +6.5%. Investors have been piling into fewer and fewer large cap growth stocks in recent years given all the uncertainty we’ve endured.

As the chart above shows, small caps have quietly kept up with large caps since May and have done particularly well post election. They may continue to find a bid if fiscal support for the economy becomes more aggressive.

Will a Weaker Dollar Boost International Stocks?

Another asset class that’s been in the doghouse in recent years is international stocks, particularly for developed markets such as Europe, Japan, and Australia. Putting it bluntly, it really hasn’t paid to invest in anything other than US stocks recently.

Growth in international markets has been subdued when compared to growth in the U.S. Both Europe and Japan have flirted with recession in the last decade, which obviously affects investment returns.

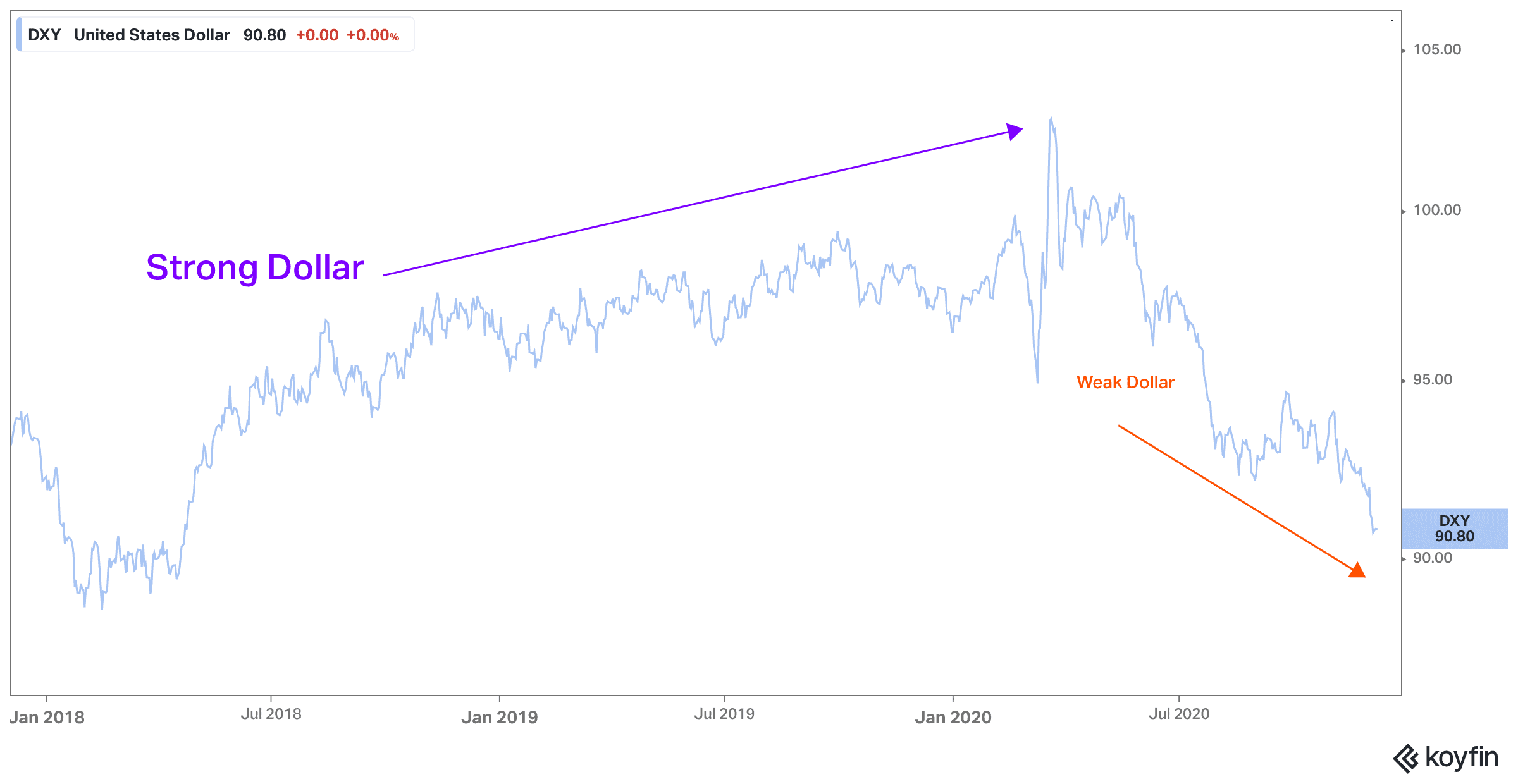

The U.S. Dollar has been strong in recent years. If the Dollar is strong, it reduces international investment returns because international currencies aren’t worth as much when converted back into dollars.

Much like small cap stocks, international stocks had a strong November after the elections. Emerging markets stocks have quietly been on a tear over the last six months, rising +25% vs. a +17% gain in the large cap S&P 500 Index.

We don’t expect economic conditions in Europe or Japan to get better soon. But as I note below, a change in posture towards more aggressive fiscal spending in the U.S. is likely dollar-negative. And if that’s the case, then it’s possible that international investing makes a comeback in 2021.

Will We Muddle Along or Try Something New (MMT)?

I’ve read hundreds of “year ahead outlook” reports during my career, and almost invariably they prove worthless by late January. It’s hard to predict the future in any aspect of life, let alone stock market returns.

But I am convinced that we’re potentially going to see a major change in the way governments approach weak economic growth. And if this happens, it will have a radical impact on the investment environment.

The global response to the Great Recession of 2008 was for monetary policy to do all the heavy lifting. Global central banks cut interest rates to 0% and they’ve been buying bonds to keep long-term interest rates low. The goal has been to entice people and businesses to borrow cheap money and spend it, boosting the economy. This plan hasn’t worked.

Now there are calls to try something new: more fiscal spending to help spur the economy. If cheap rates don’t get people to borrow and spend, then maybe direct cash payments will!

What is Modern Monetary Theory (MMT)?

The “new” kid on the economic block is Modern Monetary Theory (MMT), which we wrote about in our September 2020 newsletter. This is the driving force behind calls to significantly increase government spending in the form of stimulus and investment projects, such as green energy and infrastructure.

We cannot understate the significance of potential MMT adoption. Global central banks have waged a 40 year war on inflation. Now they’re worried inflation is too low. A major fiscal spending increase financed by central banks buying newly issued government bonds to fund higher spending has the potential to increase inflation. This is what MMT is and does, in a nutshell.

In a “muddle along” scenario, where governments continue to keep rates at 0% with modest spending, the investment environment is likely to look much the same as it has. Large growth stocks do well in that environment, while smaller stocks and international do worse.

But we now have a new Administration, and a former Federal Reserve Chair, Janet Yellen, has been appointed Treasury Secretary. This appointment fuses the spending side of government (Treasury) with the monetary side (Federal Reserve.) In short, it’s an MMT dream team.

If an MMT scenario plays out in 2021, we believe the investment environment would be dominated by inflation concerns. Large cap growth stocks could suffer, while smaller stocks do better on expectations of more support for the economy. Inflation-hedged bonds would be a big winner in that environment.

Now, After Recapping 2020 Investment Returns Let’s Discuss Investment Positioning Heading into 2021

If you read our newsletters regularly, you must excuse me for repeating a familiar refrain with FDS’s approach to investing client money. Stay well-diversified and have a disciplined portfolio rebalancing process.

2020 is probably the best real life example we have of the value of this approach. The “heat map” above gives you a snapshot of the entire year, but just a few months ago if we were recapping 2020 investment returns for year to date it would’ve looked much different.

In Spring we were buying stocks as they dropped, favoring the purchase of small and mid-sized stocks which had gotten hit hard. By mid-November, stocks had rebounded so strongly that we unwound some of these investments. We don’t buy or sell based on how we “feel” about the markets. Our investment diversification and process guides those buy/sell decisions.

Navigating around fast-moving markets takes a strong infrastructure. We have the systems in place to continually monitor client portfolios and make quick changes when they’re moving outside of their risk tolerance.

Investing is just one piece of your financial puzzle. Your financial goals are unique, so every investment plan needs a thought-out financial plan standing behind it. The financial plan is the foundation. The investment plan is the execution. Let the wild experience of 2020 encourage you to sit down with us so we can help you build that foundation.

About the Author

About the Author

Rob has over 20 years experience in the financial services industry. Prior to joining Financial Design Studio, he spent nearly 20 years as an investment analyst serving large institutional clients, such as pension funds and endowments. He had also started his own financial planning firm which was eventually merged into FDS.

Did you know XYPN advisors provide virtual services? They can work with clients in any state! View Robert's Find an Advisor profile.

Share this

Subscribe by email

11 Investment Risks You Need To Watch Out For In Your Portfolio

Good Financial Reads: Investment Education