Share this

.png?width=554&name=Copy%20of%20BLOG%20IMAGES%20TEMPLATE%20(54).png)

8 MIN READ

It’s that time of year! For the first time in two years, college campuses are welcoming students back to campus for in-person classes. That also means parents are getting bills for the Fall Semester tuition, room & board. With the cost of college where it is these days, education expenses can come as a surprise for many parents. How should parents plan for a child’s college education? How will it be paid for? That’s the topic of this post. We’ll look at:

- How the cost of college has increased over the last 25 years.

- Why you may need to change your mindset about paying for your children’s education.

- Determining how much you can realistically afford to pay for college.

- The benefits of sharing the cost of college with your child.

- Why Federal student loans may be a suitable tool to help students cover their share.

- Is a 529 college savings plan the best way to save for college?

The Cost of College Has Increased A lot!

Many of us who are parents of kids already in college know first-hand the conundrum of paying for college education. “When I went to college, it wasn’t this expensive!” It wasn’t.

For much of the 70s, 80s, and early 90s, the cost of college wasn’t too bad. Summer work and a part-time job were usually enough to pay a good portion of college expenses. But that’s changed a lot since the mid-90s.

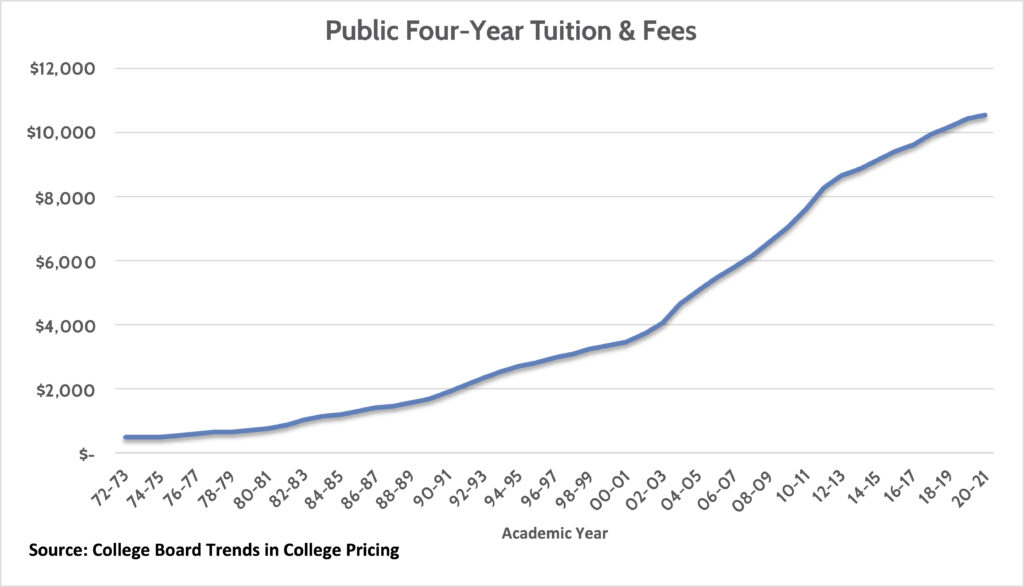

The chart below shows the average cost of in-state, four-year college tuition. It’s somewhat deceiving, however, as it doesn’t include the cost of room & board, technology, and other expenses that really add up. But it’s clear the cost has gone up a lot in the last 25 years.

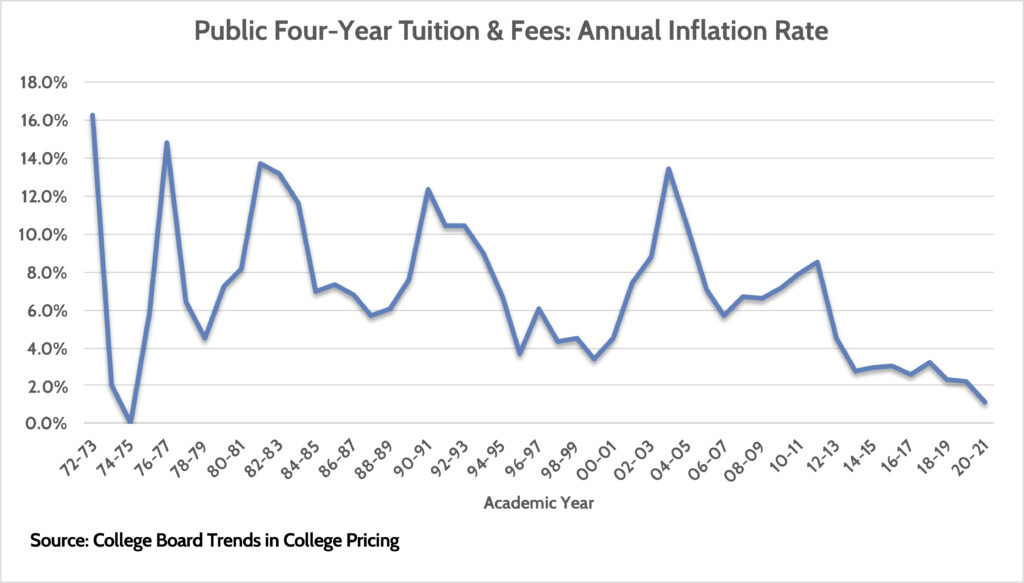

If there’s any “good” news on the college front, it’s that the rate of tuition inflation has slowed markedly in recent years. The 2020-2021 academic year saw the slowest rate of tuition inflation (+1.1%) since the mid-70s.

The reasons for this slowdown aren’t clear. But we believe it’s because parents are pushing back against the cost of sending kids to college. In the commodity world, they say, “the cure for high prices is high prices.” Meaning, if prices get too high, demand suffers, which brings pricing back down. That seems to be what’s happening.

Another reason for the slowdown in tuition inflation is the explosion in student loan debt. Recent graduates are finding that their income prospects are falling way short of what it cost them to get their degree. And they’re burdened by ridiculously high student loan debt, which impedes getting married, buying a first home, etc.

Preparing Yourself to Pay Your Child’s College Education

Adding all the above up, parents are having to re-think how they plan to send their kids to college.

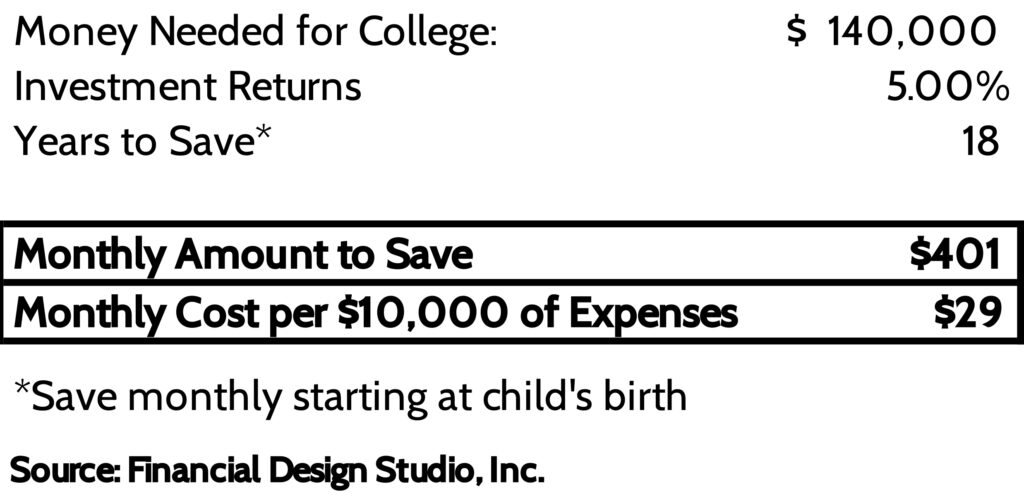

For reference, here in Illinois, it will cost a resident $35,000 per year to send their kids to the University of Illinois Urbana-Champaign. That’s $140,000 over four years!

Juggling the cost of sending kids to college with an ever-rising cost-of-living – not to mention having to save for retirement – puts many families into a bind. With that comes the need to think differently about how you plan to pay for college.

The first thing we recommend to parents planning for college is to remove emotion from the equation. Too many parents feel like they have to cover 100% of their kid’s college because that’s what their parents did for them. But times have changed. So the first thing you need to do is to adapt your mindset to today’s reality.

Once you’ve done that, you can consider some strategies we outline below. Mind you, every family is unique. These aren’t definitive answers as much as they are guides to help you think about how you can attack the problem.

Strategies to plan for a child’s college education expenses:

Strategy 1: How much room do you have in your budget to save for college?

The first thing we recommend doing is looking at your income, living expenses, and savings needs. Working with a financial advisor or a financial coach can help a lot with this exercise. Here, you’re looking at your monthly cash flow and making projections of how much you can realistically save each month towards college.

Here’s a good place to start. Using the example of our Illinois resident wanting to send their kids to Urbana-Champaign, we can figure out how much they’d need to save each month to cover the $140,000 cost. Here, they’d need to save $401 per month from the day their child was born until they turned 18!

The example here doesn’t factor in future tuition cost inflation, or the fact you may want to send more than one child to college. But you can quickly see how for most families, the idea of paying 100% of college expenses isn’t realistic.

To see how much this monthly amount would take out of your monthly budget, here’s a simple equation.

Add up your family’s Gross Income for a full year. Take out 25% for taxes. Divide that amount by 12 to get an estimate of your monthly after-tax income. Then see what percentage $401/month would be out of that. Here’s an example of how to do that.

Once you do this, you’ll quickly realize what’s realistic – and what’s not – with saving for college.

Strategy 2: Share the Cost of College With Your Child (Burden-sharing)

As mentioned before, many parents have the mindset that they have to pay 100% of college expenses. Right or wrong, that’s what we run into a lot of times when working with clients.

But if you don’t have the financial capacity to pay 100% of college expenses, it’s time to look for other options. One option is to “share” the cost of college with your child. Given the cost of college these days, having your child pay for a share of their own education is a way to give them “skin in the game.”

For example, a parent above might decide to cover 50% of the cost of their child’s college tuition. So instead of having to save $401/month for college, they’d only need to save $200/month, which is much more manageable.

The child would be responsible for the other half. If you’re clear and up-front with them starting in middle school about your intentions to cover 50% of the cost, it can incentivize them to do their best in high school.

There are tons of scholarships out there, so if they’re motivated to get good grades, join clubs, and take part in athletics while in high school, they have a good shot at winning scholarships which can help pay for their half of college expenses.

Strategy 3: Taking Advantage of Federal Student Loans

Given the student loan crisis we have, it may seem odd to advocate for students to take out loans. But if parents and students are thoughtful about utilizing loans, they can be a suitable tool for students to “bridge the gap” when paying for college.

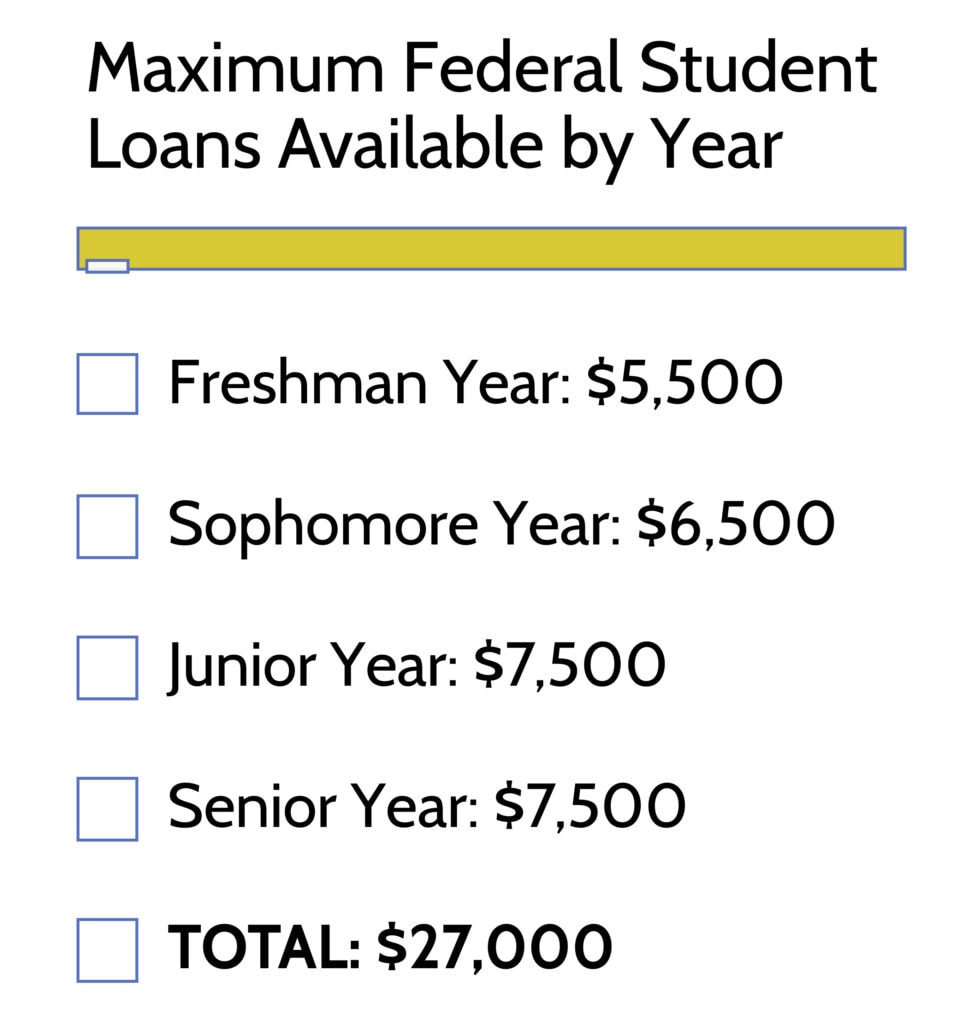

The government limits the amount of Federal student loans students can take out while they’re doing Undergrad, but these loans are lower-cost and have interesting features that may make them easier to pay off after graduation, such as loan forgiveness and income-based repayment plans.

Continuing with the example above, if a child foots 50% of the $140,000 total cost of college, then taking advantage of Federal student loans can cover almost 40% of that burden. [$27,000 of the $70,000 of expenses they’re responsible for.]

To get these loans, parents and students must fill out FAFSA forms each year they’re in school. We have a blog post that covers what FAFSA is and why it’s important. But I want to stress that ALL parents and students should fill this out each year regardless of whether or not you expect to get tuition assistance. You can’t get Federal student loans without filling out the FAFSA.

Is a 529 College Savings Plan the Best Way to Save for College?

As if figuring out how to pay college isn’t confusing enough, you also have to grapple with how best to save for college! Much like the issues we’ve discussed, there’s a wide range of opinions about whether a 529 is the “best” plan or not.

We’ve done a video that gives an excellent overview of the benefits of 529 college savings plans. From a purely mathematical standpoint, 529s make sense when saving for college. Many states allow a tax deduction for contributions to your state’s 529 plan. You get tax-free growth on your investments within a 529 plan. And if you take money out for Qualified Education Expenses, you’re not taxed on the growth in your investments.

Despite these benefits, we find a lot of parents are reluctant to use 529s. The issue that comes up is the belief that money in a 529 becomes “trapped.” What if your child gets scholarships and doesn’t need all the money in a 529? What if you over-saved? What happens if they don’t even want to go to college?!?

If you take money out of a 529 savings plan for expenses that don’t qualify as education expenses, the IRS will tax you on the growth of your investments AND issue a 10% penalty tax on top of it. Not ideal.

So what can you do if you didn’t need all the funds in a 529?

- You can bite the bullet, liquidate the account, and pay the taxes.

- Shift the 529 beneficiary to another child with no tax consequences.

- Name yourself as a beneficiary and go back to school (no tax consequences).

- Change the 529 beneficiary to a child who has student loans, allowing them to use up to $10,000 to pay back student loans.

- Leave the 529 plan in place and name a future grandchild.

You’re not “stuck” if you over-funded a 529. But there will still be parents that are wary of contributing too much to a 529. So what’s the other option?

The other option that we recommend is to open a regular taxable brokerage account. There’s no limit to how much you can put in. And you can use the funds for anything – including paying for college. In short, it’s an extremely flexible account to save for various future financial goals.

The downside is that you’ll pay capital gains taxes on investment growth when you take money out. This isn’t the end of the world, however, because if you’re a married couple filing joint taxes, you can make up to $500,000 a year and still only pay a 15% capital gains tax rate. To some parents, that’s an acceptable trade-off vs. having money get trapped in a 529.

Conclusion

Of all the financial planning topics we deal with at Financial Design Studio, college planning is always one of the tougher issues. That’s because it’s very dependent on a family’s opinions on college planning issues.

The goal of this post was to give you a framework to think about in planning for college. Knowing how much you can realistically afford is a key step. Burden-sharing with your child can be a good way to make them responsible for their education. And we’ve seen that there’s no perfect way to save and invest for college.

We always stress the point that this is ONE piece of your financial planning picture. You have retirement to worry about as well. That’s why getting a comprehensive financial plan from us is so valuable.

About the Author

About the Author

Rob has over 20 years experience in the financial services industry. Prior to joining Financial Design Studio, he spent nearly 20 years as an investment analyst serving large institutional clients, such as pension funds and endowments. He had also started his own financial planning firm which was eventually merged into FDS.

Did you know XYPN advisors provide virtual services? They can work with clients in any state! View Rob's Find an Advisor profile.

Share this

Subscribe by email

9 Benefits Of A 529 Plan

Saving and Paying for College: What Are Your Best Options?