These Related Stories

Share this

Most investors in the accumulation stage, especially where taxes are not a factor, are indifferent to whether their returns come from capital appreciation or income, as long as return (or risk-adjusted-return) is maximized.

Yet when investors move into the decumulation or spending stage, some prefer to spend only the income and have an aversion to tapping into the principal to fund their spending needs. If the annual withdrawal rate is low enough, say 2% of the total portfolio value, and assuming the portfolio holds enough stocks or other appreciable assets to combat the impact of inflation, this may be plausible given today’s stock and bond yields.

However, many investors try to draw as much as possible from their portfolio, and if their withdrawal rate is too high, trying to satisfy their annual needs with income alone can lead to problems. After considering the tradeoffs of investing for income versus appreciation, the XY Investment Solutions (XYIS) team believes that a combination of the two—the “Total Return Approach”—is most appropriate.

A Closer Look at the Income-Only Approach

Before we dive in, lets define the two sources of investment returns:

- Capital appreciation, which is an increase in the value of the investment itself, and

- Income (or “yield”), which represents payments made to the investor during the holding period, such as dividends in the case of stocks, or coupon payments for bonds.

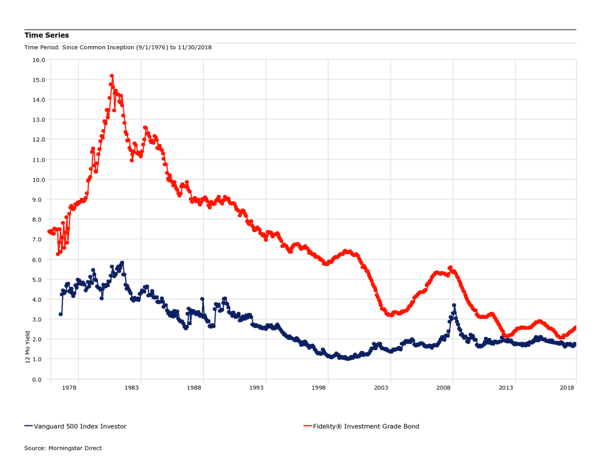

Savers and investors with experience dating back to the 1970s and 80s may recall an era when income yields on bonds and dividend yields of stocks each exceeded 5%. Simply “clipping the coupon” off their bonds and cashing their dividend checks produced an attractive income stream.

Figure 1 below shows the decline in yields of stocks and bonds since that era, using two popular mutual funds with long histories and consistent strategies as reference points. This context is helpful.

Figure 1

Source: Morningstar Direct

At today’s bond yields of around 3.0% and stock dividends around 2.0%, it is clear that investors requiring a 5% return would not meet their needs with the income alone from a diversified portfolio of investment-grade bonds and large-cap US stocks. Investors with an aversion to selling off assets (i.e. “tapping into the principal”) to accommodate their income needs often look to a number of options for boosting portfolio yield:

Option 1: Increase the Portfolio’s Allocation to Bonds

The XYIS team believes the most important decision in investing is choosing an appropriate allocation of stocks, bonds, cash, and other asset classes based on the investor’s required rate of return and tolerance for risk.

While increasing the portfolio’s weight in bonds may increase its current income, the lower total return on bonds will reduce the portfolio’s expected return, and thus the probability of meeting the investor’s goals and keeping pace with inflation.

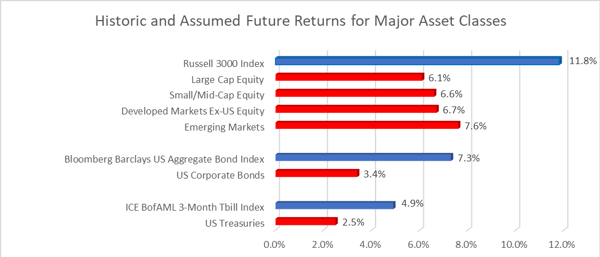

Figure 2 below shows the average annualized returns of US stocks, US bonds and a proxy for cash dating back to January 1979, as well as capital market assumptions based on a recent survey. Using sound logic and either set of data as a guide, it is evident that increasing the bond allocation will reduce long-term returns.

Figure 2

Blue bars reflect Historical Returns 1/1979-11/2018 from Morningstar Direct; Red bars reflect Average Expected Returns for the next 10 years based upon the 2018 Horizon Actuarial Services Survey

Option 2: Use Higher-Yielding Bonds

The reference points used thus far reflect broadly-diversified pools of investment-grade bonds across the maturity spectrum. It is understood that bonds with longer maturities and lower credit quality generate higher yields, leading some investors to allocate more to these segments of the bond market.

Longer-dated bonds, however, are more interest-rate sensitive, and lower-rated bonds tend to be more correlated to equity market movements, especially in times of crisis, making these categories of bonds more volatile.

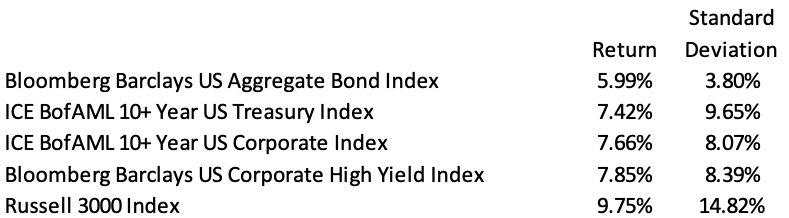

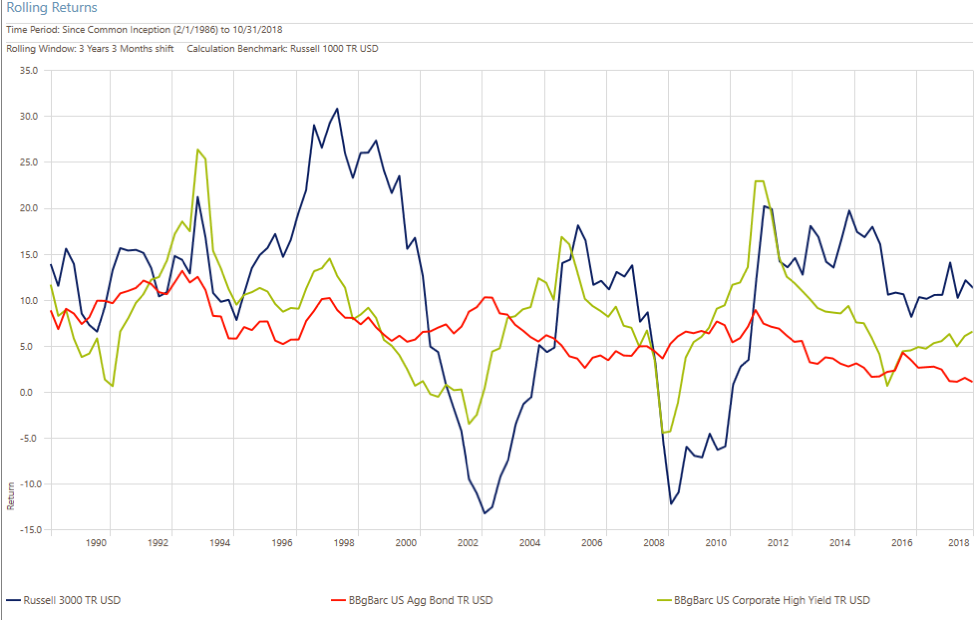

Figure 3 shows that increasing term- and/or credit risk can increase the return of the portfolio but with considerably greater volatility than a broadly-diversified bond portfolio including shorter-term securities and higher credit quality.

Figure 4 displays the similar return patterns of high-yield bonds (green) and stocks (blue) contrasted with the less-correlated nature of investment-grade bonds (red).

Figure 3 (period 4/1/87-11/30/18)

Figure 4

While adding these higher yielding segments to a portfolio can have certain benefits, we would caution against adding them simply to increase yield. Furthermore, bonds are typically used to provide a buffer against the volatility of the stock portion of the portfolio; introducing additional risk on the bond portfolio diminishes its ability to do so.

Option 3: Tilt the Stock Portfolio Toward Dividend-Payers

Dividend-paying stocks are not a suitable alternative to bonds given their volatility, so let’s just get that out of the way and revert to our assumption that the stock/bond allocation is fixed.

That said, investors in search of yield sometimes suggest allocating a greater share of their stock portfolio to dividend-paying stocks, which we think can be detrimental for a number of reasons.

First, it is important to point out that the distribution of a dividend does not create value for a company’s shareholder because the stock’s share price falls by an equal amount on the ex-dividend date.

This is difficult to observe because so many other factors influence stock prices, but from a balance sheet perspective, a company cannot just create a dividend out of thin air. If a company has $1,000,000 in cash on the balance sheet and then pays it out to shareholders, that reduction in capital must be reflected in a lower share price the next day.

This creates something of a paradox for investors who think they aren’t “touching their principal” when spending just the dividend. It’s just obscured in daily share price fluctuations.

Some investors may say they are indifferent to having, for example, a $10 stock versus an $8 stock and $2 cash dividend, and some might even choose the latter due to a “bird in the hand” preference.

We might be indifferent too, if the stock is held in a qualified account. However, if the dividend is taxable, the income approach would be inferior due to the higher tax on income vs. the capital gains if we just sold $2 worth of our $10/share holding, not to mention that the investor has less control over timing of the tax “hit” when dividends are paid versus choosing the optimal time to raise cash by selling the security.

Continuing with this example, if the investor is reinvesting dividends, not only would they be reinvesting less than the full dividend due to taxes, there may also be transaction costs associated with buying back into the security.

Another detrimental aspect to tilting the portfolio toward higher dividend-payers is that it can inadvertently skew the portfolio’s sector diversification. For example, utilities, consumer staples and REITs have the highest yields of all the sectors in the S&P, but their combined weight in the index is only 12.2%, according to JPMorgan.

Overweighting any of these would constitute a “bet” on these sectors and a bet against all the rest. Such concentration can increase risk.

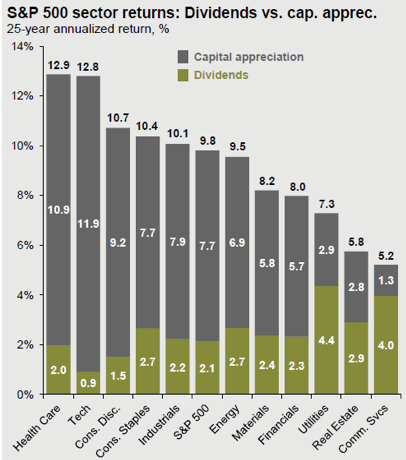

Finally, taking a dividend-focused approach may reduce the total return of the portfolio. Figure 5 below indicates that the sectors with the highest dividends were among the lowest in capital appreciation and total return over the last 25 years; on an after-tax basis, this would have been magnified.

While we cannot say this will persist going forward, it is illustrative of how a dividend-focused strategy would have led to inferior results.

Figure 5

Source: JPMorgan Guide to the Markets, 3rd Quarter 2018

Option 4: Add Non-Traditional Assets to the Portfolio

Some investors may attempt to boost portfolio yield by adding or overweighting non-traditional investments such as real estate, energy infrastructure such as Master Limited Partnerships (MLPs), or other types of strategies.

While we believe it may be appropriate for some investors to consider “alternative” investments, they should consider their total expected return, correlation with other portfolio holdings, liquidity constraints, risk of loss, and other factors before jumping in just because of a high yield.

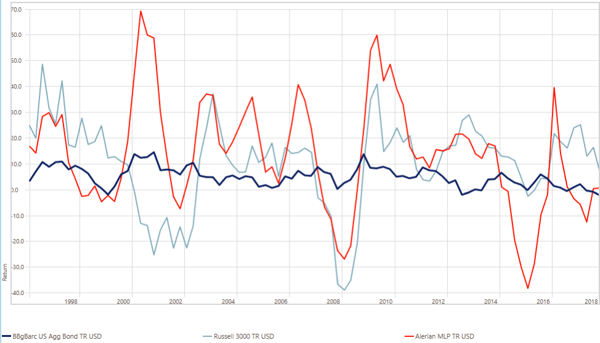

For reference, see Figure 6 for a comparison of rolling 12-month total returns for a common MLP index relative to US stocks and bonds for the period 1/31/1997-10/31/18. This is not a critique of MLPs, per se, but rather an example of why it’s important to consider the broader picture, not just the yield.

In this case, the MLP index carries a yield of around 8% today (source: Alerian), which is significantly higher than even the highest-yielding stocks or bonds; but the overall experience of an investor in MLPs would have been a wild one.

Figure 6

Total Return – A Better Approach

In a perfect world, there would be a liquid investment that generates exactly the income needed and whose principal adjusts for inflation. While inflation-adjusted bonds come close to achieving the latter, it is unlikely that their paltry yield will be sufficient to meet investor demands.

Owning appreciable assets such as stocks is one of the best ways to outpace inflation over the long-term, highlighting why they are a key component to most investors’ portfolios. As discussed earlier, however, we know that stocks’ yields have fallen over time, which diminishes our ability to spend just the income from a diversified portfolio.

Given everything we have discussed, reaching for yield comes with a variety of risks and negative consequences. Therefore, in order to meet investors’ spending needs, the XYIS team suggests constructing portfolios to achieve the maximum total return possible given an investor’s risk tolerance, even if it means overcoming his or her unwillingness to liquidate small portions of the portfolio to meet spending needs.

References and Further Reading:

-

Jaconetti, Kinniry, Phillips, 2012. Total-Return Investing: An enduring solution for low yields, The Vanguard Group

-

Horizon Actuarial Services, LLC, 2018. Survey of Capital Market Assumptions

Dimensional Fund Advisors, 2015. Yield vs. Total Return

HubSpot Call-to-Action Code

end HubSpot Call-to-Action Code

end HubSpot Call-to-Action Code  About the Authors

About the Authors

Mario Nardone, CFA

Partner, East Bay Investment Solutions

Mario began his investment career in 1999 with Vanguard mutual funds in Valley Forge, PA, where he consulted institutions and financial advisors on investment policy, portfolio construction, and Exchange-Traded Funds (ETFs). He also held roles as a research analyst, a municipal bond fund specialist, among others during his tenure.

In 2003 he earned the Chartered Financial Analyst designation, and he continues to mentor aspiring Charter candidates and young investment professionals. These experiences broadened his expertise.

Mario relocated to Charleston in 2010 to serve as Chief Investment Officer for a financial planning firm before establishing East Bay, the collaborative partner firm of (insert firm name), in 2014. As a Partner at East Bay, Mario serves a select group of Registered Investment Advisor firms as their outsourced Chief Investment Strategist.

Responsibilities of this role include continuous oversight of advisor clients’ investments, bespoke strategies for unique situations, client communications, and more. The role is multifaceted.

Mario is Past President of CFA Society South Carolina and Former Chairman of the College of Charleston Finance Department Advisory Board. His approach to investments and the industry has been featured in Investment News, NAPFA Advisor Magazine, South Carolina Public Radio, and other publications and media outlets.

Mario enjoys early morning basketball games, the Charleston beaches and restaurant scene, and spending summers in coastal Maine. He is an avid world traveler and SCUBA diver, but also enjoys the simpler joys of life with his wife Piper, their daughter Pepper, and son Santino.

Learn more and connect with Mario on LinkedIn

Eric Stein, CFA, joined East Bay Financial Services in 2018 and brings his passion for investing and client service with him. He enjoys sharing his knowledge and experiences with colleagues and clients.

Eric Stein, CFA, joined East Bay Financial Services in 2018 and brings his passion for investing and client service with him. He enjoys sharing his knowledge and experiences with colleagues and clients.

Prior to joining East Bay, Eric has worked for a variety of firms both large and small. This includes 7+ years with Goldman Sachs Asset Management where he held roles in areas such as performance measurement, client service, risk analysis and portfolio construction.

He also served as the Chief Investment Officer for RSM U.S. Wealth Management for 10+ years, providing strategic leadership and solutions for their national investment platform. This breadth of experience informs his approach.

Eric is a proud graduate of Indiana University where he earned a B.S. in Finance. He also earned the Chartered Financial Analyst (CFA) designation in 2001 and continues to stay involved in the local society.

This information is provided “AS IS” and without warranties of any kind either express or implied. To the fullest extent permissible pursuant to applicable laws, XY Investment Solutions, LLC (referred to as "XYIS") disclaims all warranties, express or implied, including, but not limited to, implied warranties of merchantability, non-infringement and suitability for a particular purpose. XYIS does not warrant that the information will be free from error. None of the information provided is intended as investment, tax, accounting or legal advice, as an offer or solicitation of an offer to buy or sell, or as an endorsement of any company, security, fund, or other securities or non-securities offering. The information should not be relied upon for purposes of transacting securities or other investments.

Your use of the information is at your sole risk. Under no circumstances shall XYIS be liable for any direct, indirect, special or consequential damages that result from the use of, or the inability to use, the materials in this site, even if XYIS or an XYIS authorized representative has been advised of the possibility of such damages. In no event shall XY Investment Solutions, LLC have any liability to you for damages, losses and causes of action for this information. This information should not be considered a solicitation to buy, an offer to sell, or a recommendation of any security in any jurisdiction where such offer, solicitation, or recommendation would be unlawful or unauthorized.

Share this

Subscribe by email

Reaching for Yield: A Careful Analysis

-1.png?width=360&height=188&name=Reaching%20for%20Yield%20A%20Careful%20Analysis%20(1)-1.png)

Reaching for Yield: A Careful Analysis

Sep 5, 2022

9 min read

The Sequence of Return Risk and the Bull Market: A Must-Have Conversation

The Sequence of Return Risk and the Bull Market: A Must-Have Conversation

Jun 11, 2018

8 min read

New SEC Rule: Document Annual Compliance Review for Investment Advisers