Saving money is difficult. I don’t think I can explain it in any other way. While we’ve developed a framework for how to help clients to think about their money and become more mindful about their spending decisions, at the end of the day, it’s always up to the individual to actually implement. This isn’t just as easy as showing someone a budget, giving them a vision for their future goals and explaining why spending less than you make is the most important part of building wealth. Even when armed with information, most people aren’t saving enough. There is a real need to change behavior and as we know from so many other aspects of our lives - waking up earlier, eating healthier, exercising daily - changing behavior is not easy.

In this post, I am going to explain why sticking to a budget is arguably the most important thing when it comes to financial success, a methodology that we (Mana) have built to help individuals and families with budgeting, as well as describe some of the things that I’ve done in my own life and with our clients to help improve behavior as it relates to spending.

Understanding your spending on an annual basis is so important.

As financial planners, one of our main goals is for clients to feel financially successful. “Feel” is the right word here, because financial success can be defined uniquely for every individual and family that strives to achieve it. The result isn’t a specific amount on a net worth statement or in an investment account; rather, it’s the softer stuff - peace of mind, reduction of stress, balance, strength, calm. Finances can be stressful. As you earn more money, things become even more complicated - financial stressors can compound. How do we simplify these problems to make them more understandable for clients? Here’s one key question from our Financial Life Design process that we think is under calculated and under asked in the financial planning world - how much do you spend on an annual basis?

Many financial advisors will simply ask a client, “How much money do you spend every year?” This just seems like such a silly question to me. “How much do I spend every year?” I have always been a math nerd and a spreadsheet nerd, but before I constructed a cash flow methodology, started crunching the numbers, tracking this and talking about it with my friends and family, I literally had no idea how much I spent over the course of the year. But the thing is, this number matters. It’s just about the most important number in determining your financial future.

Let’s say I told you I spend $120k per year, because I spend about $10k per month. Our financial planning software lets us type into the ‘expense field’ that annual spending is $120k. So what happens if I spend approximately $800-$850 more per month than expected? Well, that’s about $10k per year. If I’m in my 30s, I’ve got about 30 years until retirement, that $10k has turned into a whopping $300k ($10k x 30). If I make an assumption that the $10k was saved and invested at a 5% return each year, that $300k turns into almost 700,000 dollars!

$700,000 can be a meaningful difference between a stress-free retirement and one that is not.

$800 on a monthly basis might seem like a big swing - it’s an 8% difference from the ‘norm’. But the fact is, we see this time and time again because unexpected expenses come up. It could be anything from a child needing new sporting equipment, to a doctor’s visit that required additional tests, to a few extra dinners out because work got crazy and you didn’t have time to cook, to an impromptu trip to visit friends. The combination of any of these unexpected expenses (some within your control and some out of your control) can really add up.

For you financial geeks, the example we are about to walk through assumes inflation remains at 0% and therefore should be used for illustrative purposes only. For you saying - what on earth does that mean? If inflation were included, the amount to be saved for retirement when spending $120k per year would need to be much higher than in the example below. Furthermore, this ‘retirement number’ requires other inputs including your age today, what age you plan to retire, how long you live, and the percentage return on your investments each year.

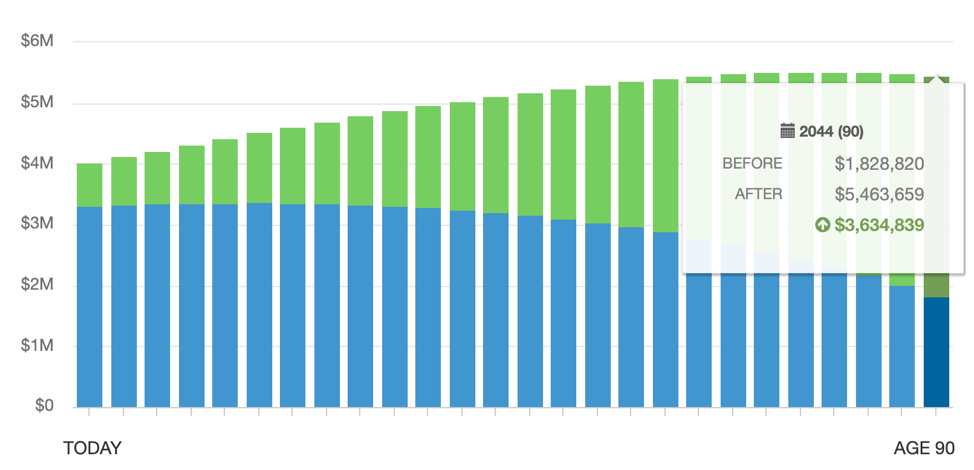

Let’s say that your financial plan projected you to retire at 65, live until 90, and earn 5% per year with $3.3 million dollars. Based on our overspending example above, what will actually result is a retirement balance of $2.6 million. This is the original projection presuming your $120k annual spend and remainder to savings, minus $700k from spending $800-$850 more per month and not investing it in a portfolio with 5% growth expectations. Now you retire with $2.6 million and you continue to ‘overspend’ vs. your $10,000 per month budget.

The result is staggering. Instead of being left with $1.8 million at age 90, your portfolio has depleted to $0 by the time you reach 81.

The chart below shows two different scenarios:

-

In the Gray = You saved $3.3 million and spend $120k per year.

-

In the Blue = You saved $2.6 million and spend $130k per year.

As a risk manager, this is what I think about. Fortunately, I have a business partner with big ideas and a growth mindset so I’ve learned that with positivity and encouragement, anything is possible. Let’s run this same example, but instead you save $10k per year extra now and through retirement, using the same 5% growth assumptions. The result is equally staggering. Instead of having $1.8 million at the age of 90, you’re left with $5.5 million! That is certainly something to aspire towards.

So how do we do this?

A few years back, I decided to quit my corporate job and go into more entrepreneurial ventures. Corporate job = regular paycheck & plenty benefits; entrepreneurial ventures = a lot less stability! When I first got started, taking away that guaranteed monthly paycheck meant that budgeting got a lot more complicated. In the past, I would proactively save and then use my credit card and pay it off 2x/month with my checking account. When my checking account got close to $1,500 - the amount where my bank would start charging bank fees - I knew that I had to slow down my spending. This wasn't an issue, because in a worst case scenario the account balance would bounce back up when I got paid every two weeks. In the new world of TBD pay check, proactively saving and using my checking account as my stop gap for my budget, I thought, wasn’t really a viable option. But this assumption was a mistake, and further analysis has led us to create five recommendations for getting in touch with your savings behavior:

#1: Normalize your income.

It’s impossible to budget if your income fluctuates. This isn’t just for those like me that decided to jump into the world of running a business. This is for anyone who has income that varies on a monthly basis.

Look out to the next 6 months and come up with a conservative estimate of what income you will be bringing in from all sources. We like the 6 month time frame because it’s far enough out to plan, but not so far that you or your business will be in a completely different place.

Have your business income or this fluctuating income deposited into a checking account. Then, set up automatic payments from this account to an account that receives a stable income of the same amount each month for the next 6 months.

Decide in advance what happens if you totally crush your income expectations. What percentage of that excess income will be saved and for what goal? What percentage of that excess income will you allocate to yourself for a bonus? Then, when you do actually crush it, you’ll have a plan in place.

#2: Make sure your essential expenses are within your means.

Write down all of the expenses you have obligations to pay on a monthly basis - the essentials of daily living. This includes your mortgage or rent, utilities, insurance, transportation costs, liability payments, any regular medical expenses, kids’ schooling, taxes and groceries. Sum these expenses and make sure that they do not exceed 60% of your normalized income. If you can keep this below 50%, even better.

If you do exceed 60%, it’s likely some changes need to be made. This can be done in one of three ways - decrease expenses, increase income, or a combination of the two.

Most of these numbers should be fixed, but we’ll talk a little more about taxes, insurance and groceries as these can fluctuate. Taxes as a result of generating income should be part of an automatic savings plan. For anyone making over $100k, put 40% of your income aside for tax purposes. If you’re over $300k, put 45% aside. In most cases, this will be more than enough, but rather have savings as illustrated in our example, than a deficit. Other taxes to consider are property taxes, which should be relatively fixed on an annual or semi-annual basis. Determine what this annual amount is and divide it by 12 to come up with a monthly budget. If you don’t have to pay it on a monthly basis, set up an automatic transfer to a savings account to help cover these costs when they are due. Similarly for insurance, if you are paying on a semi-annual or annual basis, come up with a monthly number and proactively save. For groceries, we find that estimating a weekly number is easiest to come up with a good monthly budget. When you’re at the grocery store, keep this weekly number in mind so you can hold yourself accountable to not overspend.

#3: Proactively think about and write down your future plans.

As a lover of travel and gift giving, I tend to overcommit. However, since I started monitoring spending for myself and other families, I’ve noticed that one of the biggest drivers of confusion to the monthly budget are the actual costs of trips and the gifts that we give to others throughout the year, especially around the holidays.

For travel, write down all of the trips that you have planned for the next 6 months. If you’re a big planner, do this for the next 12 months. If you don’t precisely know your plans, try to come up with reasonable expectations of where you might go (e.g. East Coast / International Trip) and what these costs could entail. Write down all of the costs of flights, hotels, transportation, restaurants, gifts, and activities for each trip.

What’s nice about this exercise is that you can check yourself to make sure that your plans are reasonable, but also - the sooner you plan and book your trips, the less money you will likely spend on these trips. Last minute purchases can be costly, so if you know that you travel for the holidays or other occasions every year, use some of the resources below to help you strategize and be proactive about making plans.

-

Google Flights. A super easy way to price flights with filtering for airlines, dates, times and class of service. You can even track flights, see how the cost compares to average, and receive email updates on prices.

-

Scott’s Cheap Flights and Next Vacay. These are email lists that are sent on a daily basis that give you flight deals to & from places around the world. You can set your ‘home airport’ and where you want to go and you’ll get emails with this information. I find this useful in two scenarios: 1) if you love to travel and have a list of places you’d love to go, but you have some flexibility on when; and 2) if you know where you want to travel and it’s far into the future, you can use this to find deals that you might not find if you book on another day.

For you gift givers, write a list of all of your family, friends and charity for whom you want to buy gifts in a given year. This is also a great time to put all of your family and friends’ birthdays in your calendar with reminders a week in advance, so you won’t forget. If you are in a phase of life that weddings are prevalent, estimate the number of weddings you’ll be attending. Put down a budget for what you would like to spend next to each of your recipients and see what this amounts to on an annual basis. Divide by 12 - and you’ve got your monthly gift giving budget.

#4: Automate your savings

Once you have your income locked in and you know that your essential expenses are less than 60% of your take home income (income net of tax), and you’ve proactively planned, automate your savings.

We put together a chart to help depict a simplified bank structure that we’ve described in the sections above.

You already know that you should be saving for:

-

Taxes

-

Insurance annual payments

-

Travel & Gifts

But what else?

If you have specific goals in mind to save for - this is great - but for those of you who find it challenging to come up with your goals, it’s not necessarily an essential starting point. We love goal setting at Mana and it’s a huge part of the work we do with clients, but it really does involve a deeper exploration of what’s important to an individual or family, not just a simple exercise that we can write in a blog.

Thrive Global recommends to build a system rather than staying so laser focused on goals, because the system will actually propel you to achieve your goals. This concept fits well with today’s piece. Come up with an amount between 10-20% of your normalized income that you feel comfortable stashing away into savings. Set this up as an automatic transfer into a savings account and/or brokerage account. You will see results.

#5: Simplify and prioritize what’s most important to you with the rest.

If you got lost in the mix of the numbers above, use 20% of your normalized income as your starting point for simplification and prioritization. If you’re still with me, take your remaining balance for this exercise. Here’s a little summary to help.

When you first get started, 20% of your take home income can seem like an extreme goal. And frankly, it is! I think this is probably the most challenging part about budgeting - if you don’t have a need to budget right now, then doing so can get pushed off to next month...every single month.

However, I can tell you from experience that necessity can drive you to make changes that you didn’t think were possible. Having been a person who went to the nail salon 2x/month, bought iced coffee everyday, bought take-away lunch every weekday, and spent $300/month on endurance related fitness classes, I can tell you - I considered each of those expenses as essential in my budget. As an entrepreneur, I paint my nails, make my own coffee, prep lunches at home and go running outside several times per week. That is my $800 - or my $700,000 in 30 years. A small daily sacrifice for a big reward.

I challenge you to use January 2020 as your test for the 20%. Over the next 2 months, figure out your take-home pay or normalized income. Multiply it by 20%, and use that as your fun / lifestyle budget for the month of January.

Some tools you can use...

-

Try the extreme. In my case and in the case of friends that I asked who I know have gone through financial hardship, we had to adopt the rule of “Does it cost money? OK, then it’s too expensive.” We had this dialogue with every purchase made outside of essential expenses. Once I started turning things down, I reaped the positive reinforcement benefits of my own intrinsic strength and will-power!

-

Understand the why. Ask yourself the 6 questions mentioned in this video by Dr. April Benson when making a purchase: Why am I here? How do I feel? Do I need this? What if I wait? How will I pay for it? Where will I put it?

-

Find an accountability partner. Encourage family and friends to do this with you. Money conversations should be free of shame and fear, but unfortunately our society tells us that talking about money is taboo. Accountability is so important when it comes to changing behaviors. Explain how important this is and why you want to do this together with someone. You’ll be amazed how many others have the same desire to spend less.

This blog went through some strategies we use to help people budget in their own lives, but ultimately it comes down to changing behavior. When it comes to spending, you can generally have anything you want, but you just can’t have everything. I hope some of these strategies can help you improve your relationship with your budget and how you save before ever needing to do so.

About the Author

About the Author